By Kevin Nicholson, CFA, Global Fixed Income Co-CIO, Co-Head of Investment Committee. SUMMARY We believe the Fed’s actions should not derail investors before it begins raising interest rates. We believe the trend and sentiment both suggest proceeding with some caution.Collectively, the three tactical rules still point to a pro-risk allocation, in our view.

Source: Original Postress-this.php?">The Three Tactical Rules Remain Bullish, but Proceed with Caution

Last weekend, Novak Djokovic attempted to capture the calendar grand slam in tennis by winning the US Open, after already winning the Australian Open, the French Open, and Wimbledon earlier in the year. Djokovic fell short in his quest and now our three tactical rules are attempting their version of a calendar grand slam: signaling pro-risk for the entirety of 2021. As we begin to close-out the third quarter, we explore the status of “Don’t Fight the Fed”, “Don’t Fight the Trend”, and “Beware of the Crowd at Extremes” which appear to be painting the lines (shots that land on the lines); still pro-risk but proceeding with caution.

Don’t Fight the Fed: (Serving Up an Ace)

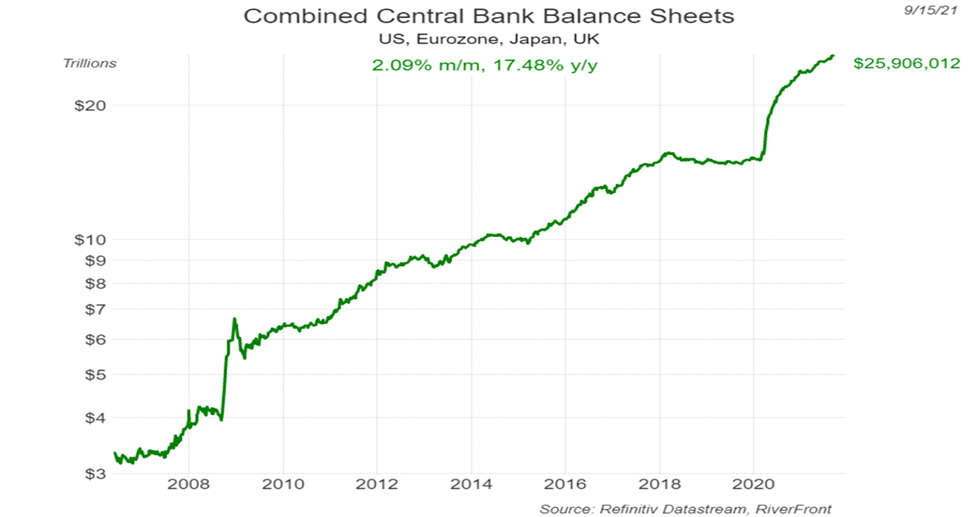

Since the beginning of the year, the Federal Reserve (Fed) has grown its balance sheet by just over $1 trillion. In June, the Fed increased the rate that it pays participating banks to 5 basis points, in order to soak up excess liquidity. Additionally, the Fed has stated it will delay raising interest rates, even though it is planning to begin tapering its $120 billion purchases of Treasuries and mortgage-backed securities sometime before year-end. While we acknowledge tapering will make the Fed less accommodative, we believe they will still be printing money for a period of time and will still be acting in investors’ best interest by delaying rate hikes. Therefore, we believe the Fed is still on investors’ side regarding monetary policy.

Similar to the US, most international central banks have started talking about tapering, but have yet to trim their money-printing programs. Of the major international central banks that we follow, European Central Bank (ECB), Bank of England (BOE), and the Bank of Japan (BOJ), only the BOJ has not considered any form of tapering. Despite international central banks considering tapering, they have not done so and remain on investors’ side, as illustrated by the chart below:

Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

Central banks around the world continue to serve up aces for investors, in our view. When a tennis player serves an ace – an unreturnable serve – their confidence builds, and by keeping rates low, we think central banks are signaling to investors that it is okay to have a higher risk profile and invest in equities.

Don’t Fight the Trend: (Swinging Away at the Baseline)

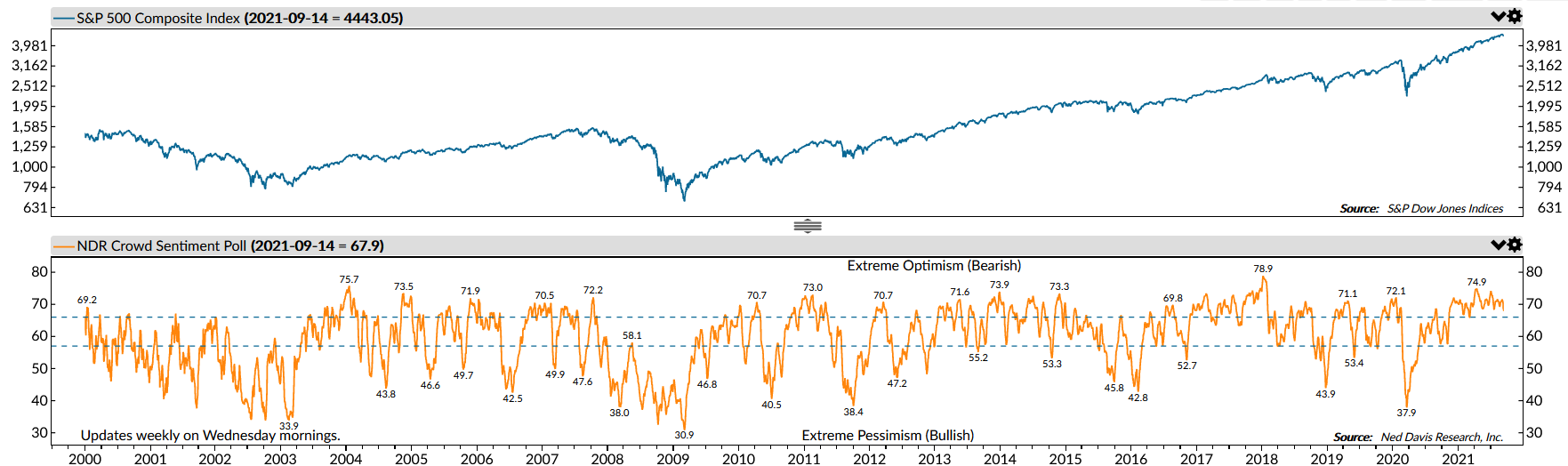

We define the US primary stock market ‘trend’ as the 200-day moving average of the S&P 500. Currently, the trend in the US is rising at an annualized rate of 35%, an extraordinarily strong slope which we believe is unsustainable for long periods of time. However, through the lens of our proprietary trend heatmap, the strength of the trend is still pointing to positive future returns over the next 3 months. While we continue to watch the trend cautiously, its positive momentum has helped the S&P 500 continually make new highs. The international trend represented by the 200-day moving average of the MSCI All-Country World-Ex US Index, on the other hand is at a less extreme 20%.

Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

Given the strength of the trends domestically and internationally, we would compare this to a tennis player standing at the baseline trying to keep the ball in play, increasingly aware that too strong of a swing could cost them the point.

Beware of the Crowd at Extremes: (Double Faulting)

The Crowd has been riding high this year as it has benefitted from strong earnings growth, supportive Fed policy, and government transfer payments in the US. As the economy has reopened from the pandemic, the Crowd has remained in the extreme optimism zone. The elevated level of crowd sentiment has concerned us for all of 2021, as we recognize that at some point the music will stop and the party will end. We believe that sentiment at extreme optimistic levels sets investors up for disappointment, similar to the letdown a tennis player feels when they double fault. At current levels, looking at crowd sentiment in isolation would prompt us to reduce the level of equities in the portfolio.

Copyright 2021 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at http://www.ndr.com/copyright.html. For data vendor disclaimers refer to http://www.ndr.com/vendorinfo/.

Conclusion:

Unlike Djokovic, we place greater odds on our three tactical rules achieving the rare calendar grand slam, as collectively they still point to a pro-risk portfolio positioning. The Fed and global central banks are accommodative, the trend is positive and growing rapidly, and excessive crowd optimism is being worked off by the current pullback. In keeping with these conclusions, the balanced portfolios currently have equity allocations that are 6 to 7 percentage points higher than the composite benchmark allocation.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.