All news seems to be bad news, with such a broad consensus that the market and economy are headed for trouble.Yet, earnings are better than expected, and the economy is showing more signs of resilience.Despite the negativity, we are on track for a soft landing, which is why stocks continue to climb the wall of worry.

The Market And Economy Continue To Defy Bearish Forecasts

All news seems to be bad news, and if there is good news, no one wants to hear it. I have never seen such a high level of conviction from the consensus that the worst of a bear market is in front of us and that a recession will inevitably follow. I see two fallacies in this narrative. The first is that expectations for such doom and gloom are so widespread that they are largely factored into valuations. The second is that the historically reliable indicators for economic contractions that bears are leaning on have been triggered by anomalies in this unprecedented post-pandemic business cycle. Furthermore, the stock market has now grinded higher for six months, defying all bearish forecasts. It is no coincidence that the bear-market low coincided with the peaks in inflation and long-term interest rates. Stocks have climbed as both have fallen, as markets respond to positive rates of change.

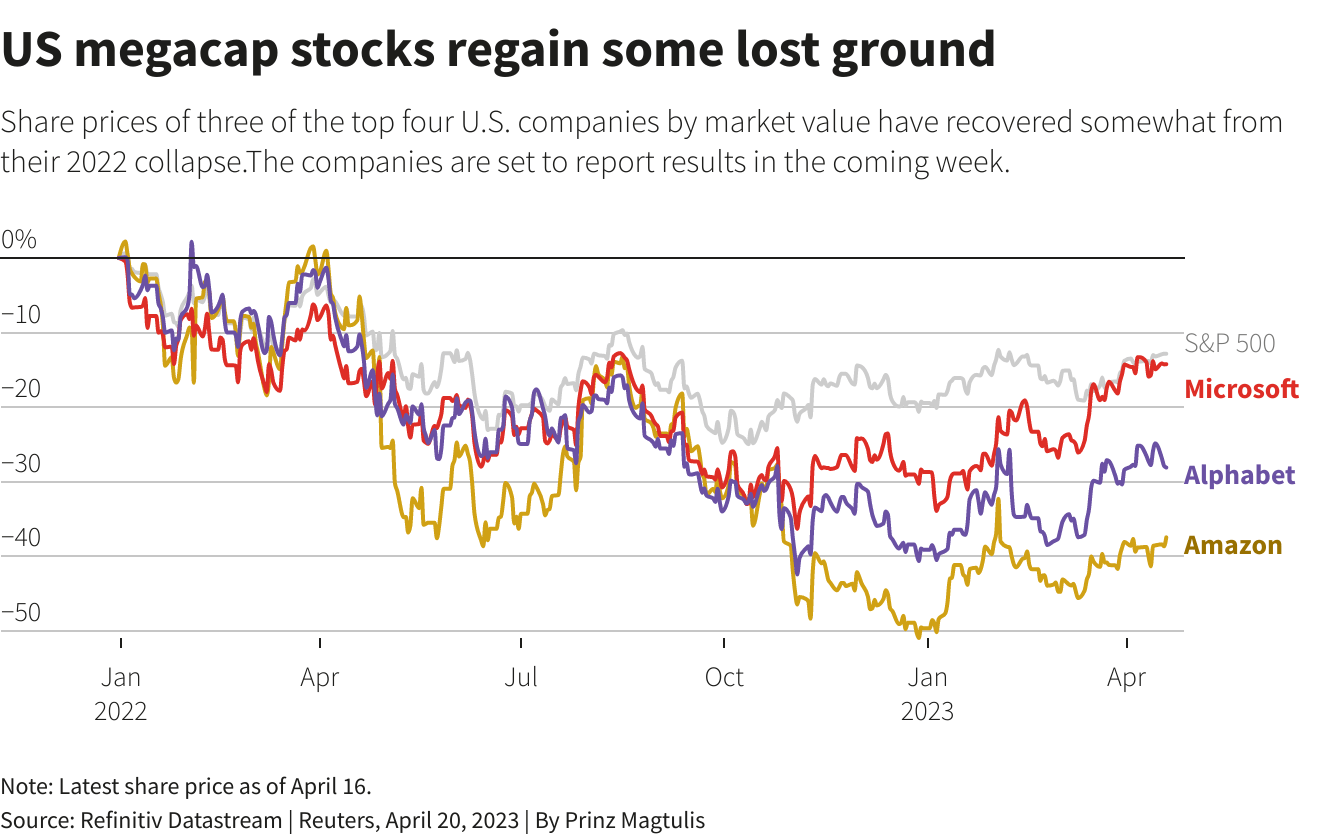

Wall Street’s top market strategist and leading bear pointed out last week that the rally in the S&P 500 has been driven by a handful of the largest companies, with the percentage of stocks outperforming the index on a three-month rolling basis at its lowest level on record. Morgan Stanley’s Mike Wilson asserts that this means the bear market is far from over. Yet what he fails to acknowledge is that the largest names in the index are simply catching up after months of underperformance.

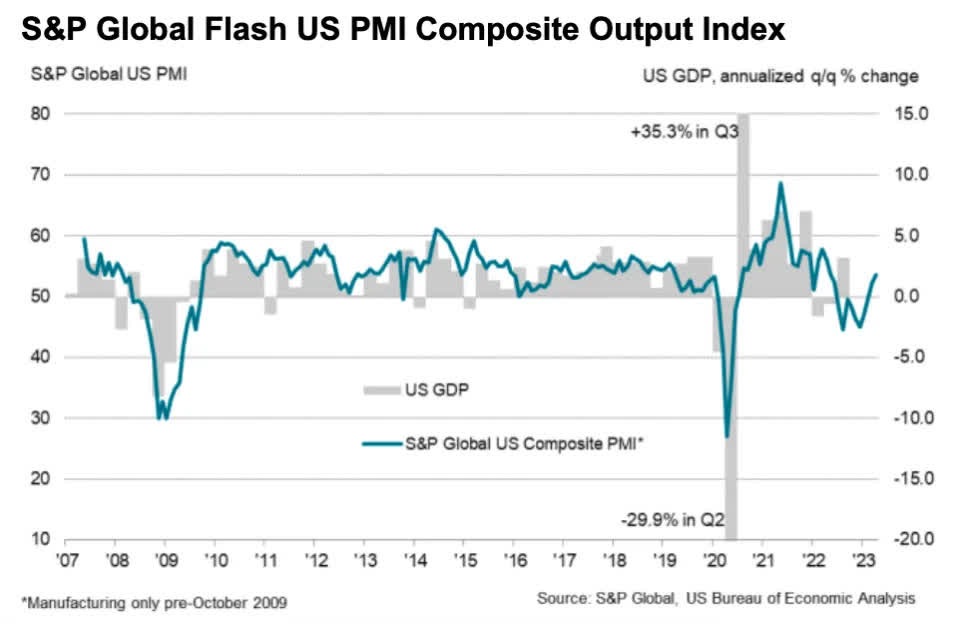

There have been signs that tighter financial conditions are starting to slow the rate of economic growth, but a recession still does not look likely in 2023. S&P Global’s mid-month index of economic activity for April rose to an 11-month high in Friday’s report. This rebound comes after seven months of declines and is consistent with GDP growth of better than 2%. The index rose from 52.3 in March to 53.5, and it was not driven primarily by the service sector.

Strength in the manufacturing sector rose to a six-month high, as demand for goods is starting to recover. We saw the first signs of this in the New York Fed’s regional survey of manufacturing activity last week. This suggests to me that inventories have been worked down after consumers spent months focused on services spending. S&P Global’s manufacturing index rose from 49.2 to 50.4, which signals a return to growth.

This is what needed to happen to keep my outlook for a soft landing on track, but it will also revive fears that the Fed must keep raising interest rates in its quest to reduce the rate of inflation to 2%. Again, all news is likely to be construed negatively until the economy has safely landed with price increases falling close to the Fed’s target.

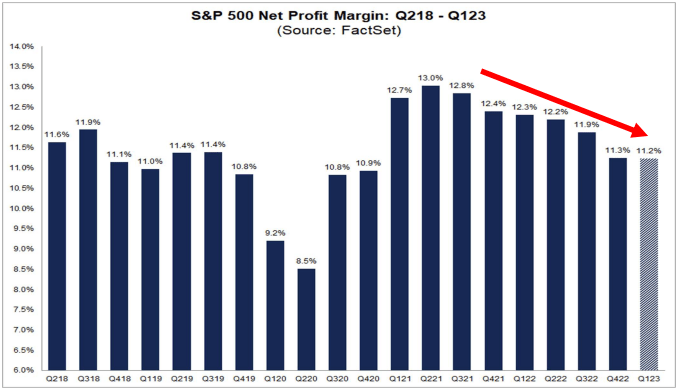

This week, we have 170 constituents of the S&P 500 reporting first quarter earnings. According to FactSet, the consensus estimate was for a 6.7% decline in profits on March 31, but that has improved to a 6.2% decline after results from approximately 18% of the index. I expect to see a continuation of that improvement this week, as the cost-cutting efforts from 2022 combined with declining input costs are protecting margins to a greater extent than expected.

In fact, while margins have declined for six consecutive quarters, they appear to be returning to pre-pandemic norms rather than collapsing as some pundits have suggested. Margins were at unsustainably high levels. The disinflationary environment we are in today is a tailwind. This earnings season should be the catalyst that takes the S&P 500 into bull market territory.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.