Andres Victorero

The Vanguard Total Bond Market Index Fund ETF (NASDAQ:BND) is a good alternative to US Treasuries for investors looking to take advantage of high nominal and real yields while limiting the duration risk in exchange for some credit risk. At 4.8%, the yield to maturity on the BND is now almost a full percentage point higher than 10-year US Treasuries. While the fund has a weighted average maturity of 8.9 years, compared to 8.3 years for the iShares 7-10 Year Treasury Bond ETF (IEF), its duration is lower at 6.5 years versus 7.5 for the IEF. This limits the risk posed by the ongoing and extreme inversion of the US yield curve.

I argued in my previous article on the BND that the ETF was highly likely to outperform US stocks over the coming years, and the recent rise in the BND’s yields advantage strengthens this case. The BND is also likely to outperform corporate bonds over the coming months and years.

The BND ETF

The Vanguard Total Bond Market ETF tracks the Bloomberg Aggregate Float-Adjusted Bond Index. The BND has a history of being less volatile than similar maturity US Treasuries as the exposure to credit risk limits losses during economic booms and limits gains during recessions. This credit risk has also seen the Bloomberg Aggregate Float-Adjusted Bond Index outperform Treasuries over the long term. While the ETF is dominated by US Treasuries, it also has substantial exposure to securitized and industrial bonds. The fund charges a minimal expense ratio of just 0.3%.

4.8% Yield Makes BND Ripe For Outperformance

I expect the BND to outperform US Treasuries, US stocks, and corporate bonds over the coming years for the reasons outlined below.

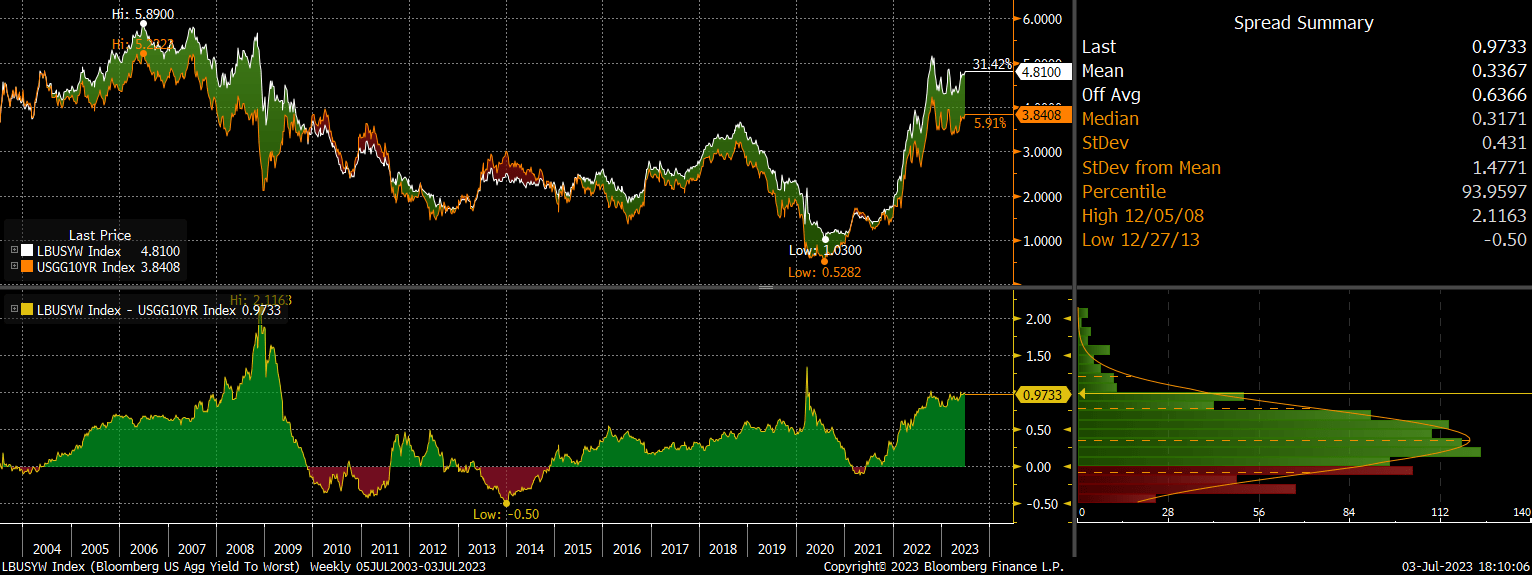

Versus US Treasuries: The BND’s yield is highly favorable when compared to similar maturity US Treasuries, with the yield now 97bps higher than the 10-year UST yield. Over the past 20 years we have only seen this spread higher at the height of the Covid credit crunch and the Global Financial Crisis.

US Aggregate Bond Index Yield Vs 10-Year UST Yield (Bloomberg)

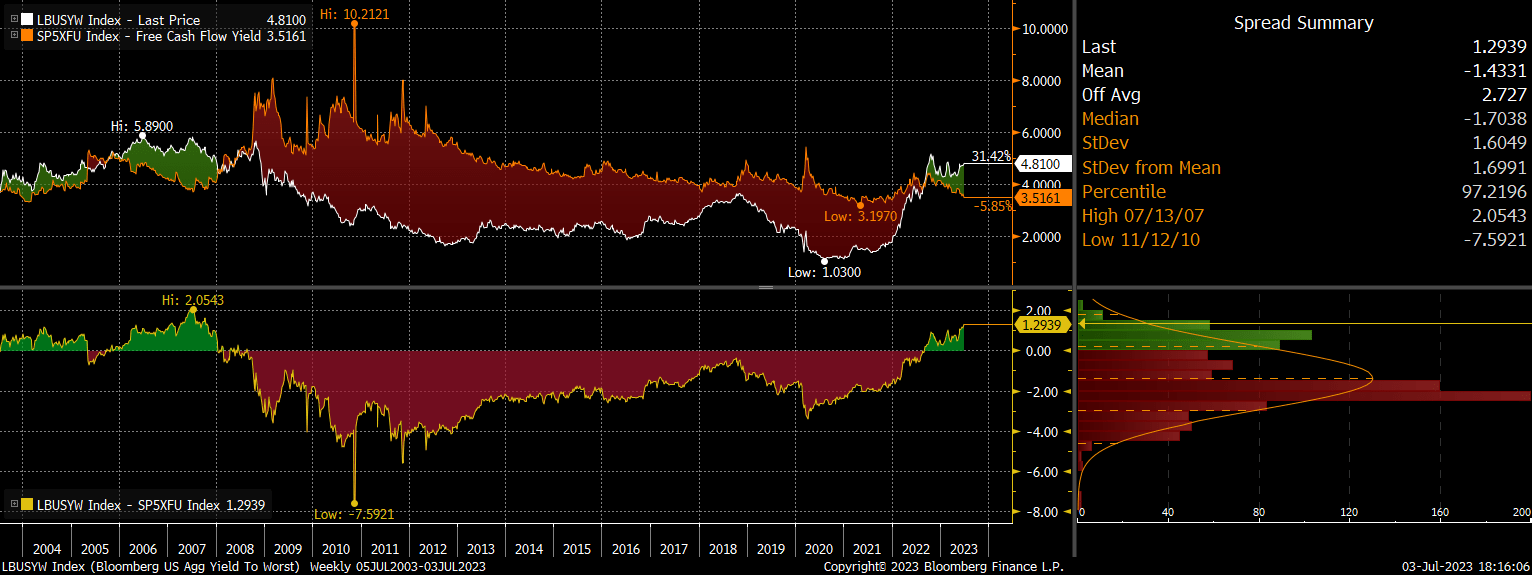

Versus US Stocks: The return outlook for the BND has also further improved relative to US stocks over recent months, with the yield now 1.4x and 1.3pp higher than the free cash flow yield on the S&P500. This is the highest yield advantage since the peak of the S&P500 in 2007.

US Aggregate Bond Index Yield Vs SPX FCF Yield (Bloomberg)

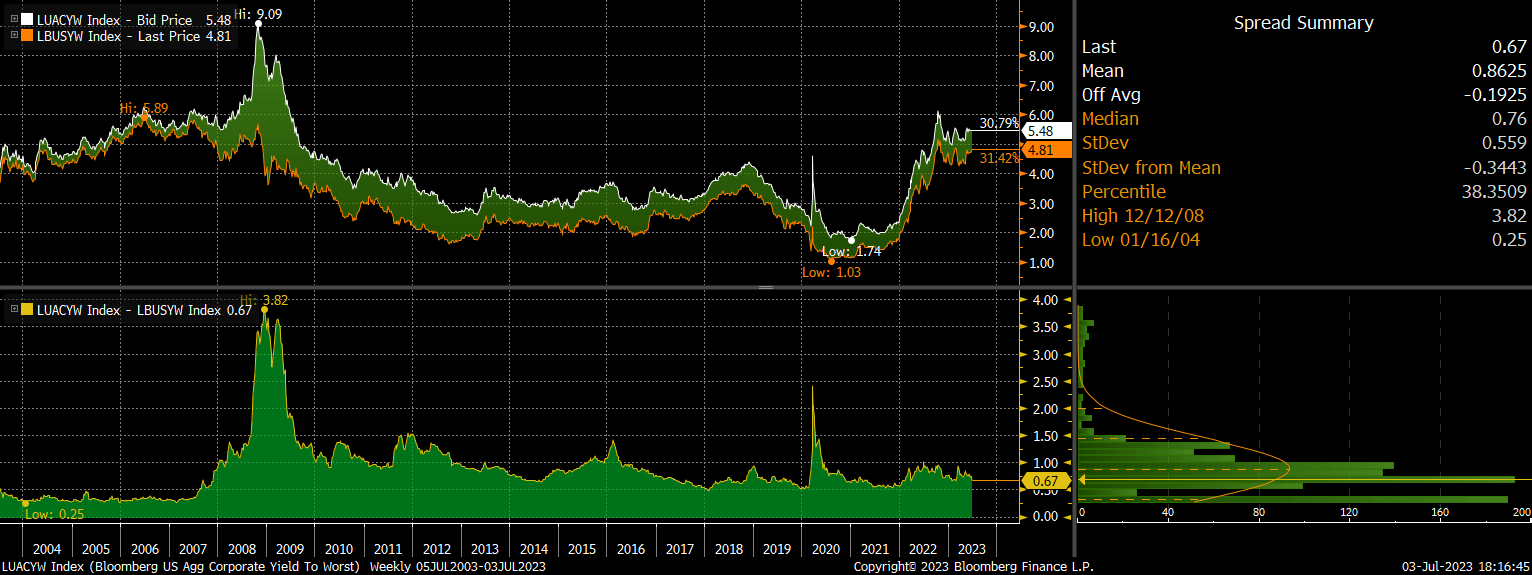

Versus Corporate Bonds: I also believe that the BND’s outlook is strong relative to corporate bonds over the coming months and years. The yield on the Bloomberg US Investment Grade Corporate Bond index is now just 67bps higher than the yield on the BND’s underlying Bloomberg Aggregate Float-Adjusted Bond Index, which is historical low. This leaves corporate bonds much more exposed to a spike in risk aversion.

Corporate Bond Index Yield Vs Aggregate Bond Index Yield (Bloomberg)

Yield Curve Inversion Warns Of Exposure To Interest Rate Risk

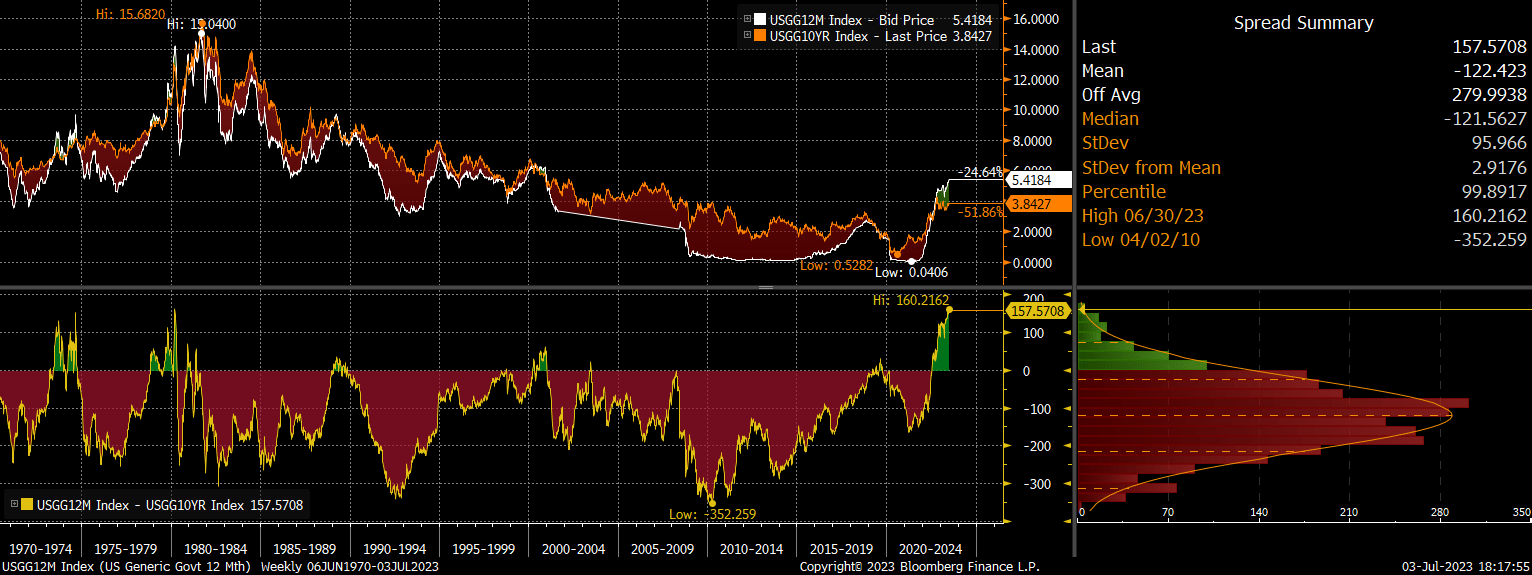

The BND is also much less risky when compared to similar maturity US Treasuries due to the lower duration. As I noted in ‘EDV: Long-Term Bullish But Near-Term Risks Rising‘, the ongoing rise in short-term bond yields heightens the risk of a near-term rise in long-term yields as the yield curve is now extremely inverted. 12-month bonds now yield 157bps above 10-year bonds, which is the most extreme steepening seen over the past 50 years.

12-Month vs 10-Year UST Yield (Bloomberg)

While it is true that periods of yield curve inversion have previously normalized via falling short-term yields which also drag down long-term yields, we cannot guarantee history repeats this time. With stocks continuing the shrug off higher yields, the Fed may be forced to continue hiking, leading to a rise in yields across the curve. With the exposure to corporate bonds reducing the BND’s duration relative to similar maturity Treasuries, the BND is less exposure to such a rise.

Why Not Just Buy Short-Term Treasuries?

With the yield curve so inverted, investors do not actually have to take on any credit risk and or duration risk to generate high income. The Fed funds rate itself is now higher than the yield to maturity on the BND, as is the yield on the iShares 1-3 Year Treasury Bond ETF (SHY) which also has zero credit risk and very little interest rate risk. That said I still prefer the BND to short-term Treasuries as I ultimately see the Fed funds rate falling significantly over the coming years as real GDP and inflation continue to weaken, which should provide capital gains to the BND.

A Credit Crunch Represents The Main Risk

The main risk to the BND comes from a credit crunch. Despite the heavy weighting of Treasuries, the BND has seen sharp selloffs during periods of intense credit market strains in the past, as gains from rising USTs have been offset by losses on industrial and securitized bonds. That said, losses in 2008 and 2020 were short lived and gave way to strong subsequent returns.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.