Introduction

While much of the publicity of the healthcare industry revolves around pioneering new life saving therapies, new frontiers cannot be manifested without proper research instrument technological advancement. As the foundation of the healthcare industry, life science tools are essential for modern biopharma companies to operate, and companies such as Thermo Fisher Scientific, Inc (TMO), Danaher Corporation (DHR), and Agilent Technologies, Inc (A) highlight the lucrative opportunities that exist. Remove any of these companies from existence, and we would reverse decades of scientific advancement.

However, the giants of the industry do suffer from oversaturation of the market, with issues of oligarchy outshining the honest R&D being performed and developed (even in 2024 we hear that the FTC is heavily scrutinizing Thermo’s necessary growth M&A deals). If the issue continues, will we see regulation against the giants and how can investors avoid this risk?

For me, I believe diversification is the first and foremost factor for investors, no matter the case. This is especially true as I am a long-term oriented investor searching for recurring investment opportunities with my monthly savings. Therefore, I believe taking risk by investing outside of the traditional safe haven opportunities may play out well in the future. As many may say, I am looking for the next generation of Thermo Fishers and Danahers. To date, I have covered the highest quality opportunities of the moment with three key holdings:

-

Bruker Corp (BRKR) – For their dominance in advanced nuclear magnetic resonance technologies, and growing conglomeration of next-gen analytical instruments. Despite a low $12 billion market cap, BRKR has a long history of profitable growth.

-

Bio-Techne (TECH) – For access to the highly profitable, secular growth opportunity in life science reagents and consumables for leading research use. At a $10 billion market cap, there remains plenty of room to grow.

-

Revvity (RVTY) – The best value for a growing life science and diagnostic conglomerate, with financials that will reflect the larger peers of DHR and TMO moving forward after restructuring the business.

In the coming months, I personally will be reallocating my healthcare exposure to these names as the pillars of growth for the future. However, I will also be allocating some diversification to even smaller, more innovative companies to benefit from niche and novel technologies. So far I have only discussed Cytek Biosciences (CTKB) as the best exposure to the rising need for spatial and single-cell visualization techniques.

In this article, I will highlight a similar company that instead focuses on first to the market expertise in mass spectrometry, 908 Devices, Inc. (NASDAQ:MASS). With three main platforms for growth, the primary opportunity of 908 Devices is with secular bioprocessing 4.0 needs. According to GEN, Bioprocess 4.0 can be summarized as follows:

Bioprocessing 4.0 is a reality. It is part of a broader movement known as Industry 4.0, which is, essentially, the fourth industrial revolution. The idea of the fourth industrial revolution was introduced about 10 years ago, when German researchers suggested that manufacturing should exploit cyber-physical systems. Soon, the idea was popularized by World Economic Forum leaders who emphasized that cyber-physical systems were blurring the lines between the physical, digital, and biological spheres.

In the years since, many industries, including the automotive and electronics industries, have been moving decisively toward Industry 4.0. However, the biopharma industry has lagged behind.

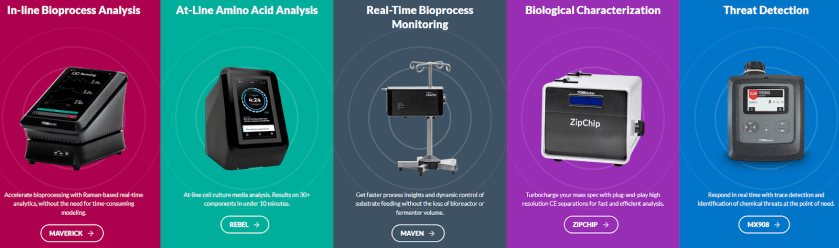

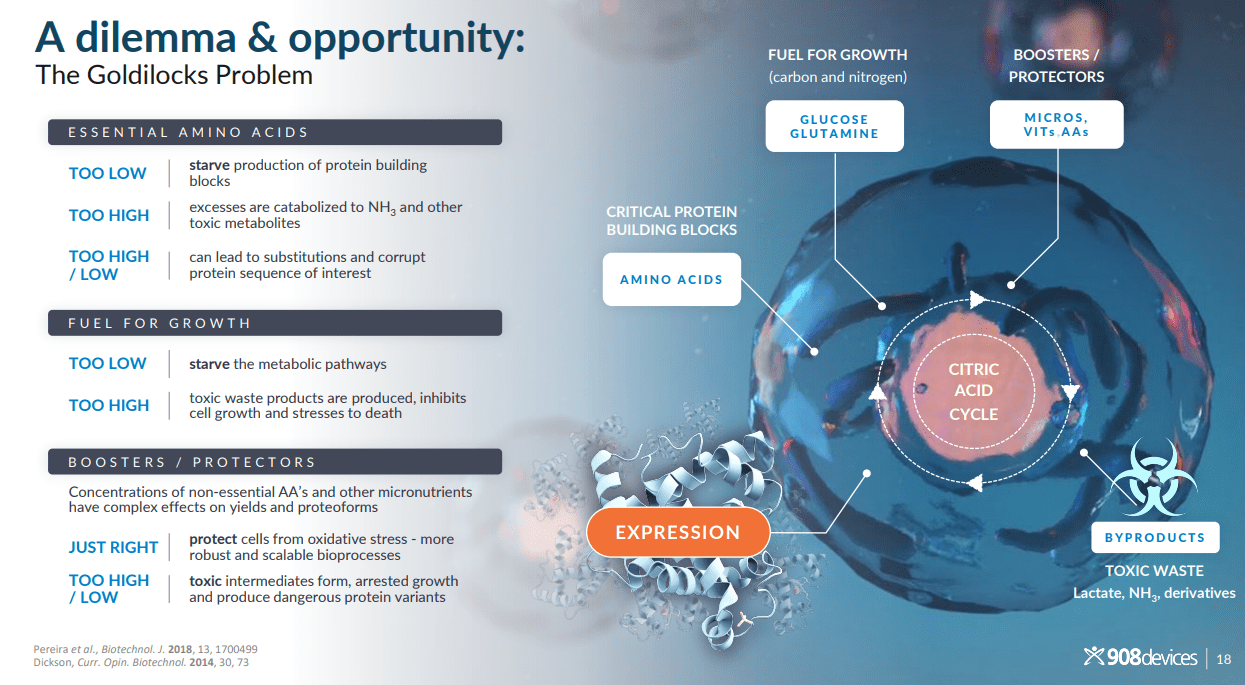

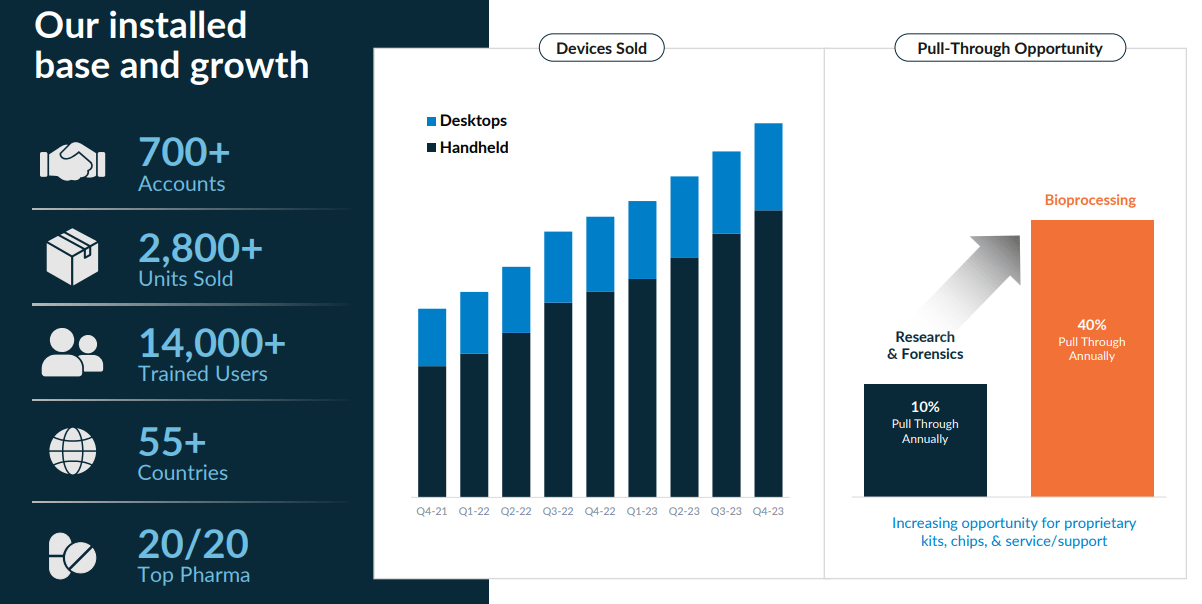

Data integration and analysis are where 908 Devices shines, thanks to advantages in usability and efficiency. The first product, the MX908, is a portable mass spectrometer for use in primarily forensic situations, but can easily handle rapid quality assurance duties in the lab. However, these products are more niche due to pricing and will remain focused on the forensic industry, where they are being well received. Instead, I see the primary platforms for 908 Devices future to be the bioprocess analysis tools of Rebel (at-line), Maverick (in-line), and Maven (on-line).

These devices are used to analyze bioprocess samples at three stages, at-line (remove a sample during the process), in-line (continuously analyze the process during operation), and on-line (continuously analyze via automatic removal without contaminating or disrupting the process). An additional innovation for CE-MS, the ZipChip, is also sold by MASS and can be integrated into a wide variety of partnered instruments from Thermo Fisher, Danaher’s SCIEX, and Bruker.

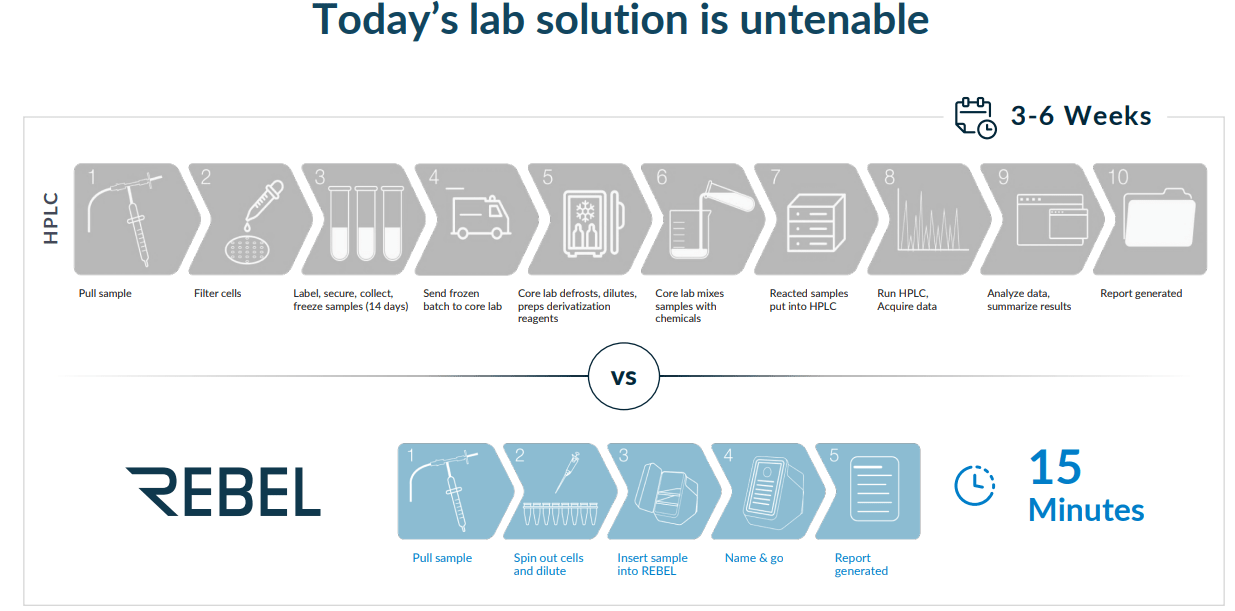

MASS are pushing the Rebel as the star of this segment, with management touting the device as being able to complete a similar high purity liquid chromatography sample analysis that takes 3-6 weeks in only 15 minutes (assuming the customer has to outsource analysis). As an at-line analyzer, customers only need to take a sample at some point in the process and rapidly analyze the constituents of the sample. Speed is created by using miniaturized sample preparation and separation IP that is on a scale far smaller than any other MS platform.

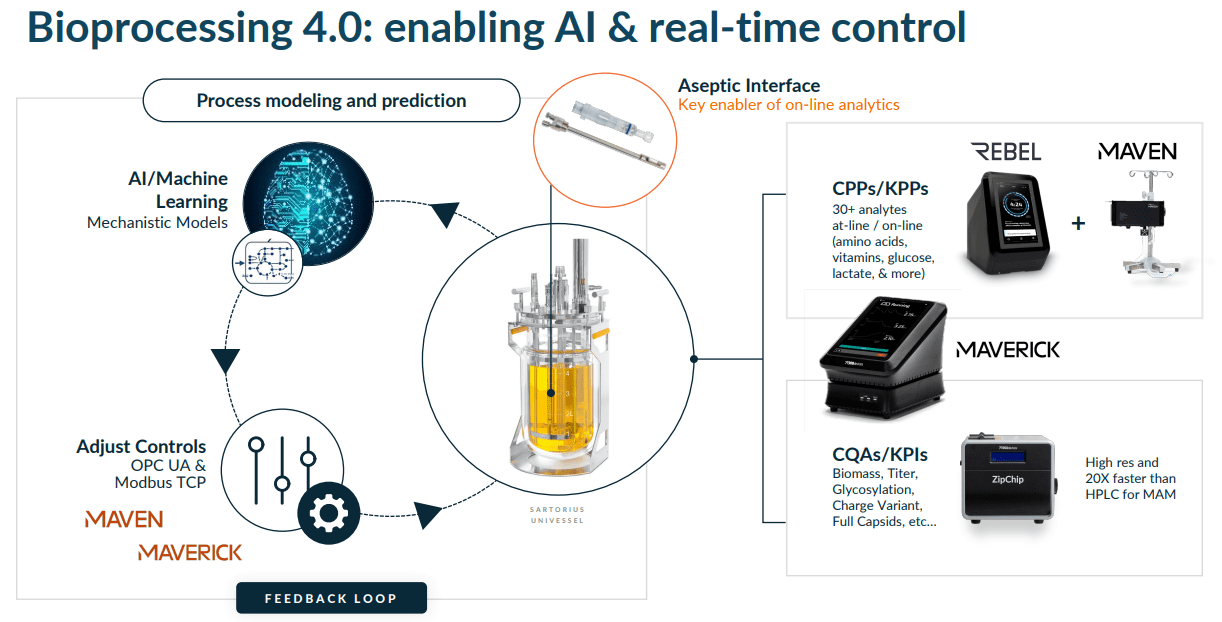

Rebel can also be combined with Maverick’s continuous monitoring and Maven’s automatic solution control systems to provide customers with a new wealth of bioprocess knowledge to increase efficiency and control. And to date, the success of the platform has already been established through a partnership with global bioprocess tech manufacturer Sartorius.

908 Devices Website

908 Devices Presentation

908 Devices Presentation

908 Devices Presentation

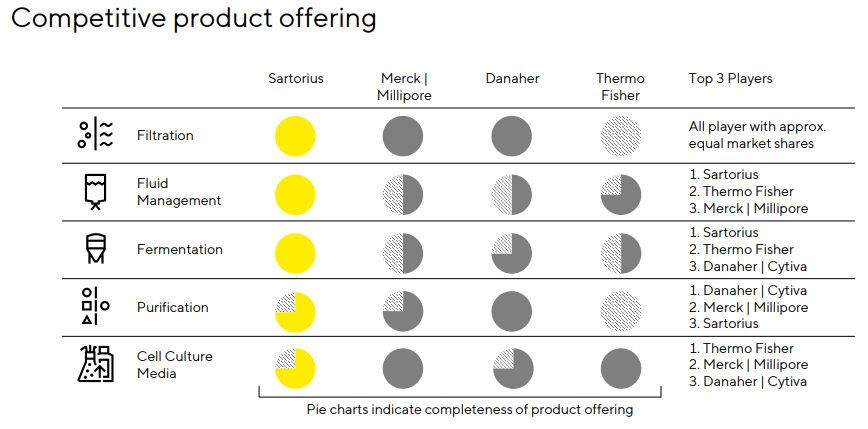

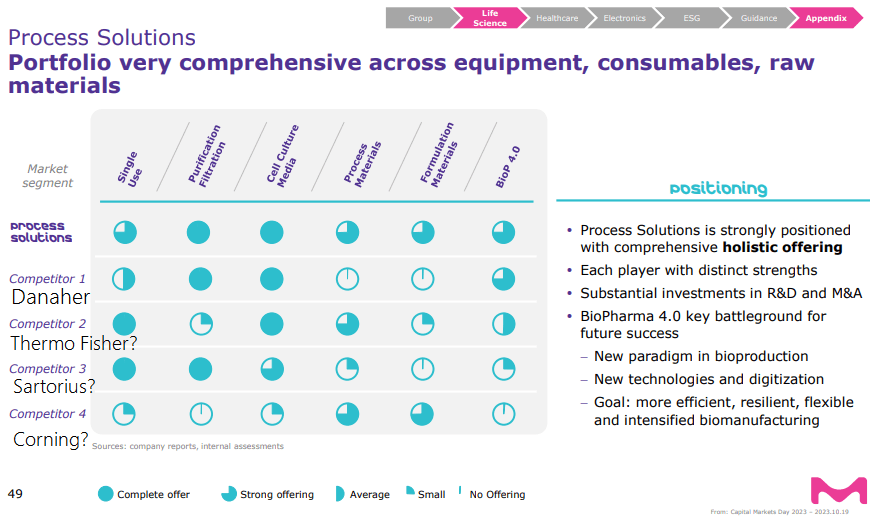

Competitive Landscape

These products are essential for the success of Industry 4.0 in Bioprocess and will allow biologic drug manufacturers to optimize the bioreactor environment for efficiency and quality in the face of high costs and regulatory pressure. I have already discussed how 908 Devices has a first-mover advantage in the space, but competition is fierce. There are four major players in the industry: the aforementioned Thermo Fisher, Danaher, Sartorius, along with MilliporeSigma of German Merck KGaA (OTCPK:MKKGY). The key dynamics can be assessed with competition matrices published by Sartorius and Merck, along with the table I created on company performance below.

Firstly, each company has areas where they shine, with no clear leader across the entire bioprocess suite. This has led to all bioprocess customers needing to work with all industry participants, rather than working with a single partner. It is also clear that Merck and Sartorius believe they will be the first to provide full scale solutions, despite TMO and DHR leading the sale of consumable-type products. With 908 Devices already working with three of the majors, TMO/DHR/SARTF, it is clear that a future runway is available for MASS to grow even if Merck or others increase competitive offerings. This is especially true with Bioprocess 4.0 becoming the next battlefield as indicated in Merck’s competitive chart. Therefore, I look positively to MASS’s current competitive position thanks to the current partnerships in place, even if 908 Devices fails to become industry standard equipment moving forward.

Sartorius Investor Presentation

Merck KGaA Presentation

Bioprocess Market Update

908 Devices’ products are well positioned to capitalize on future bioprocess investments and market growth, but what is the current market outlook? In 2024, the market remains well into a bear-cycle despite high levels of FDA approvals for biologic therapies. This is because the pandemic led to an incredible bull run for the industry, and high interest rates have reduced expenditures. As such, all the major companies, and including bioprocess upcomer Repligen (RGEN), have seen large declines in revenues over the trailing twelve month period. However, long-term growth rates remain elevated above typical healthcare sector levels, with all bioprocess segments seeing at least high single digit, if not greater, revenue growth prior to the pandemic.

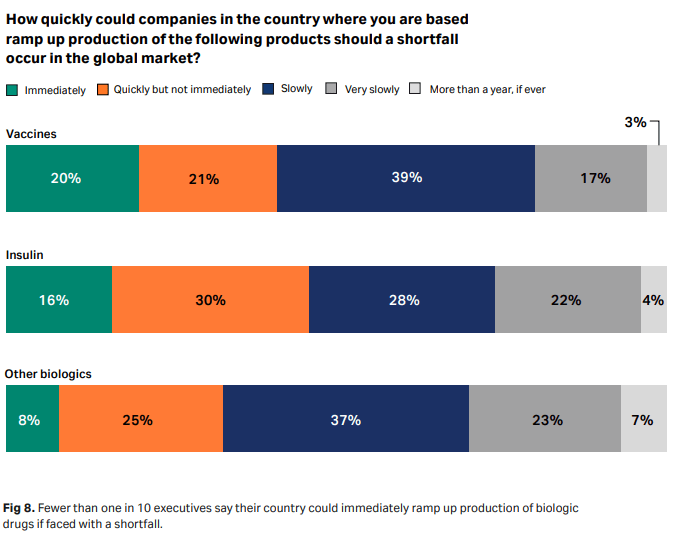

What is driving this low-lying secular opportunity? Primarily, the need for better and safer therapies via biologics. Secondly, diversification of the manufacturing base for these biologics. As such, it is not just biopharma that is acquiring bioprocess tech, but the wide range of contract organizations that are outsourcing the production process. Evidence for this can be seen by a recent industry leader survey done by Danaher’s Cytiva subsidiary that highlighted current market sentiment on bioproduction capability globally. Of note, over 60% of respondents believe that biologics manufacturing will be slow to ramp up in the event of a global shortfall, more than other biologics such as vaccines and insulin.

As the globe invests to solve this issue, the need for efficient processing will allow 908 Devices to thrive. So far this year, growth has remained positive despite the broader slowdown. Based on current outlook and guidance by the majors, I would not be surprised if MASS can sustain above 10-15% revenue growth indefinitely as they gain a footing. Upon maturation, sales will be in-line with the market, which is suggested to be the high single digits by the majors. In particular, the field of cell and gene therapy is expected to provide significant secular opportunity for the bioprocess field, and the more complex a therapy, the more likely that MASS’s products prove useful. I would look at Repligen’s mid-teens growth rate as a more viable growth comparison for now, so investors can look forward to that.

Cytiva

|

Company |

Bioprocess Market Sales |

TTM Segment Growth Rate |

Market Growth Expectation (Mid to Long Term) |

|

Thermo Fisher |

~$4 billion | BioProduction (process) ~30% of $12 billion LS segment |

-26 |

Long term Mid teens EPS growth on 7-9% core organic market growth across all divisions. |

|

Danaher |

~$3 billion | ~50% of $7.1 billion Biotechnology Segment |

-18 |

Low single digit decline for 2024 and high single digit long term core growth. |

|

Sartorius |

$3.0 billion | Bioprocess 80% of $3.7 billion total revenues |

-19 |

2024 mid to high single digit growth |

|

Merck KGaA |

$4.1 billion Process Solutions Segment |

-14 |

Low teens for Process Solutions |

|

Repligen |

$639 million |

-21 |

10%+ annually mAbs and 20%+ annually Biosimilars mAbs and Cell, Gene, and RNA therapies |

|

908 Devices |

~20% of $50.2 million |

7.2 |

4-8% revenue growth in 2024 |

Table 1: Compiled by Author with Company Data.

Financial Update

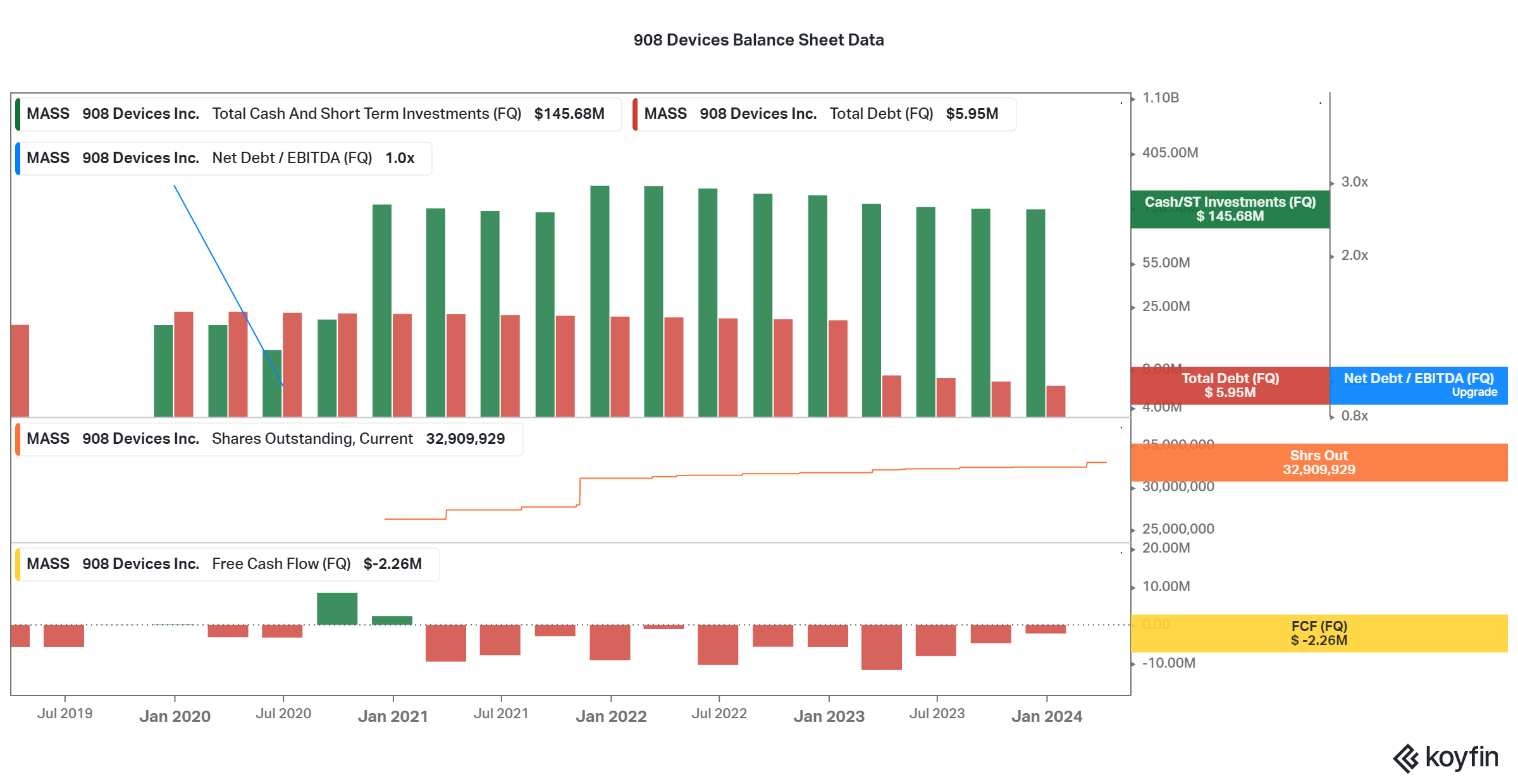

Financially, 908 Devices has found solid footing despite operating at a loss. Quarterly cash losses have maxed out at around $12 million in 2022, while cash on hand is at $145 million last quarter as per the Koyfin data charted below. And, the last four quarters have begun to show FCF losses improving linearly. This provides at least three and a half years of runway for the company to become profitable, and if the trend continues, positive FCF generation may occur in the next few quarters. However, margins are still negative to account for the necessary spend on expanding the platform. Many investors may be averse to investing in a loss-maker, but the technology looks promising as long as the operational runway allows for some flexibility.

I believe that if the market begins to return to normal, profit generation can occur, and this may occur within the current operational runway bounds. Sure, more debt and dilution may be an issue until profit generation is stabilized, but if successful, capital gains will be far more significant. In particular, the rising proportion of desktop sales highlights the opportunity for higher ARR/pull-through, which suggest a profitable state can be achieved similar to other recurring revenue companies. See my recent articles on Revvity, Bio-Techne, or Cytek for more details.

908 Devices Presentation

Koyfin

Conclusion

At a $220 million market cap, 908 Devices is beginning to show value as well. In particular, a EV/Sales less than 2.0x at 1.54x is favorable for long-term investors, as I usually see 4.0x or below as a solid entry point for innovative loss-makers. The full P/S is close to that level at 4.2x trailing sales, so I believe it is worth taking MASS into consideration. I will personally be using the company as a speculative growth lever alongside the other proven winners in healthcare. I will also only be using profit generated from low-risk assets to fund my speculative investments, and I hope this provides successful capital growth in the years to come.

Thanks for reading. Feel free to share your thoughts below.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.