Dzmitry Skazau

As the U.S. Presidential election draws nearer, many investors are eyeing the future of the soon-to-expire 2017 Tax Cuts and Jobs Act- a significant individual tax code overhaul that reduced taxes across income levels-and more specifically, its potential impacts on the municipal bond market. Although each possible election outcome will likely result in different tax scenarios, municipal bonds are set to maintain their tax-equivalent-yield advantage no matter the outcome.

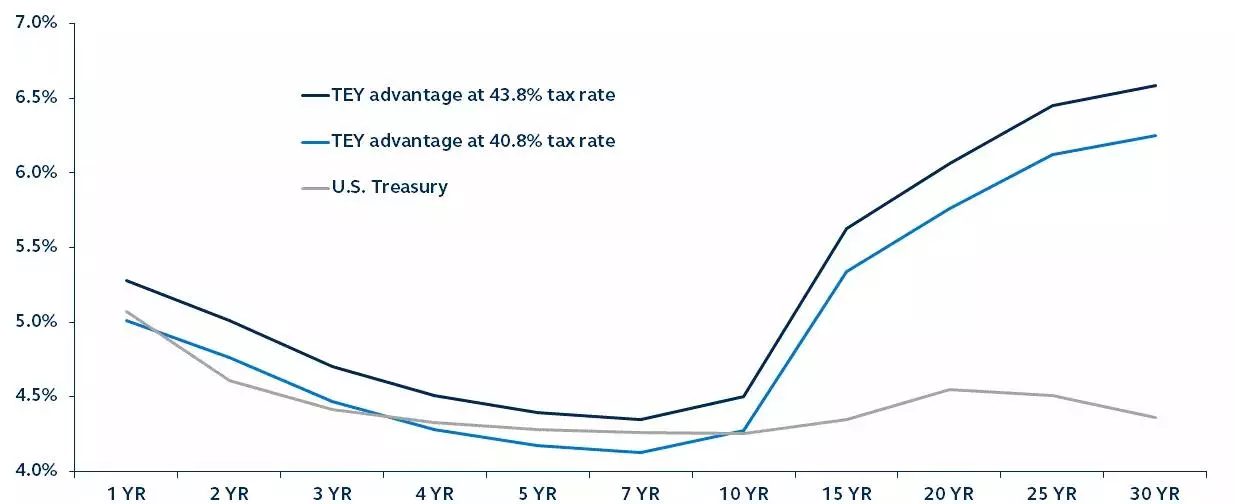

Taxable equivalent yield (TEY) advantage of municipals at different tax rates – TEY by maturity

Source: Bloomberg, Principal Fixed Income. Data as of February 29, 2024.

The upcoming Presidential election is increasingly capturing the market’s attention. One of the most significant policy issues is the future of the 2017 Tax Cuts and Jobs Act (TCJA), an individual tax code overhaul that reduced taxes across income levels, set to phase out in 2025. Its sunset presents crucial fiscal decisions for the next administration, and each election outcome is likely to have implications on municipal bond markets:

- Divided Government: The TCJA likely expires, raising tax rates for all-notably, top earners, with a hike to 40%. This would boost demand for tax-exempt municipals as exemptions become more valuable. The corporate tax rate would likely rise as well, increasing demand from taxable buyers (e.g., insurance companies).

- Democratic Sweep: Municipal demand would grow with expected increases in individual and corporate tax rates, aligning with President Biden’s proposals for higher taxes on wealthy individuals and corporations.

- Republican Sweep: The status quo likely persists, with the TCJA’s cuts extended, maintaining the top rate at 37% with minimal impact on tax-exempt municipal demand. On the taxable side, demand would remain low. Even at 37%, the TEY advantage that municipals offer is significant.

Regardless of the election outcome, the ever-increasing federal deficit underscores the importance of revenue, with individual income taxes remaining a primary source for the U.S. This is unlikely to change, and individual tax rates are unlikely to move lower. In fact, the opposite is more likely, further enhancing the value of the tax exemption and leading to greater investor demand for the municipal asset class.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.