For the past 15 years, large-cap stocks have significantly outperformed small caps, and with good reason. Initially, they were a safe haven from risks following the 2008 financial crisis, benefiting from the zero-interest-rate policy that allowed larger companies access to long-term, low-cost funding. More recently, the largest companies, known as the Magnificent 7 (Alphabet (GOOGL), Amazon (AMZN), Apple (AAPL), Meta (META), Microsoft (MSFT), Nvidia (NVDA), Tesla (TSLA)), have been pioneering the technologies of the future. Most importantly, the foundation of their outperformance has been a period of exceptional large-cap earnings, which rewarded large-cap investors.

This dominance persisted through 2024, yet market breadth narrowed considerably. During the first half of the year, these seven stocks accounted for more than half of the S&P 500’s total return. However, with the recent volatility across equity markets, we are seeing signs that a new leadership may be on the horizon.

Is it time to get back into small caps? Here are three reasons we think now is the time for investors to think about allocating to stocks of smaller U.S. companies.

1. Benefiting from a soft landing

Based on the recent upward revision of U.S. second quarter GDP and the Atlanta Fed’s GDP forecast for the third quarter, the U.S. economy continues to show resilience. Meanwhile, incoming data suggests that inflation is largely behind us. Altogether, these indicators suggest the Fed has successfully engineered a soft landing.

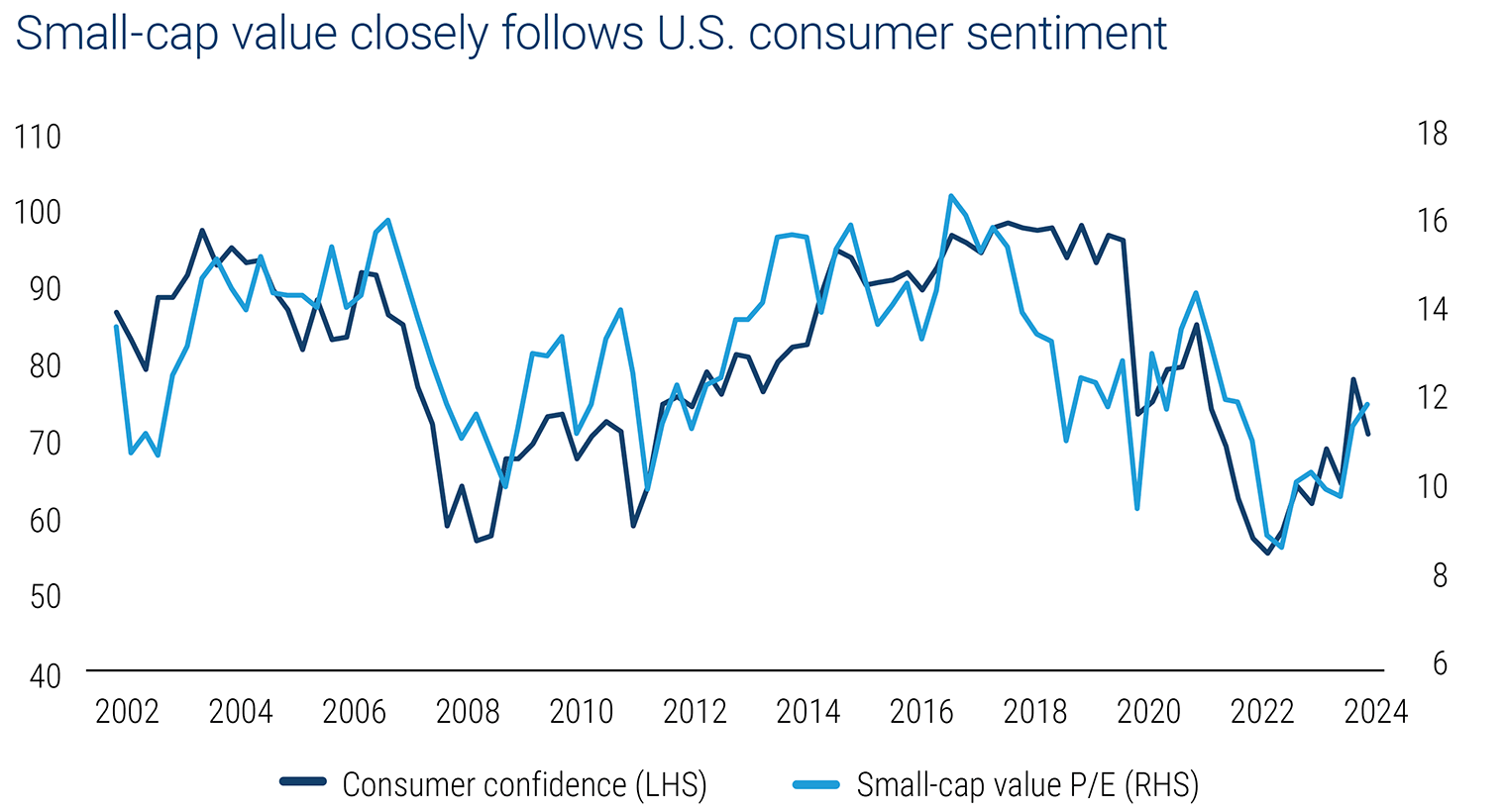

Why is this so important? With 80% of small-cap company revenues coming from domestic sources,1 the health of the U.S. economy directly impacts their earnings potential. One indicator of the strength of this relationship is the high correlation between consumer sentiment (as represented by the University of Michigan Consumer Sentiment Index) and small-cap value valuations.

Source: FactSet, University of Michigan: Consumer Sentiment, retrieved from FRED, Federal Reserve Bank of St. Louis. Quarterly data. Consumer sentiment is represented by the University of Michigan Consumer Sentiment Index, and small-cap value valuations are represented by the Forward P/E of the Russell 2000 Value Index. As of April 2024. An investment cannot be made in an index.

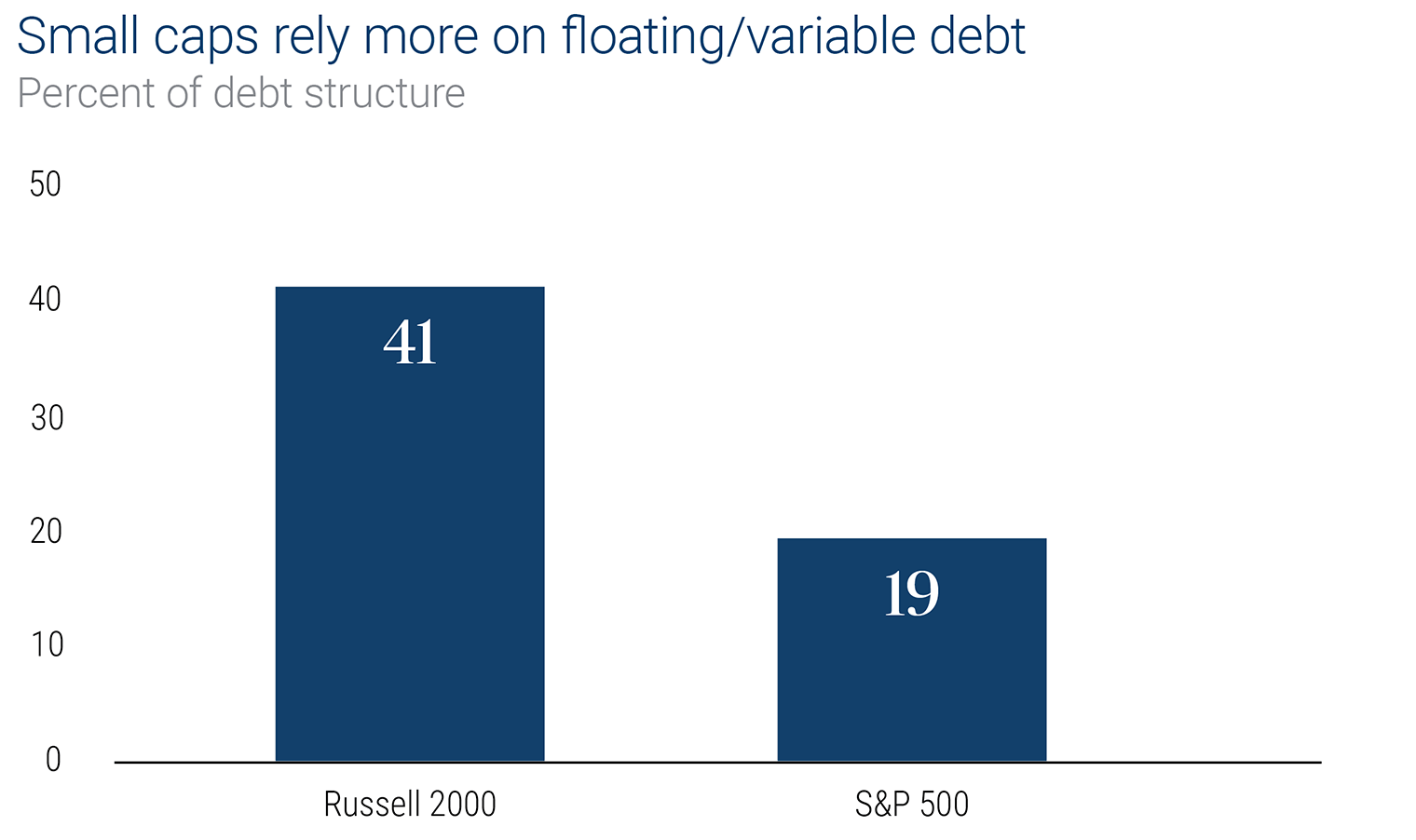

With much of the developed world bogged down by stagflation, the durability of the U.S. economy stands out. This strength is expected to continue, driven by significant investment in domestic industries, particularly artificial intelligence. Should economic growth remain robust, we may be entering a phase where small-cap earnings surpass large-cap earnings, starting in the fourth quarter of 2024. Not only are fundamentals expected to improve during this period, but this strength is also anticipated to align with the Fed’s easing cycle. While we expect the long end of the yield curve to remain anchored, short-term interest rate cuts will provide relief to some smaller companies with floating-rate debt.

Source: Columbia Threadneedle Investments as of August 31, 2024. An investment cannot be made in an index.

2. Small caps are undervalued

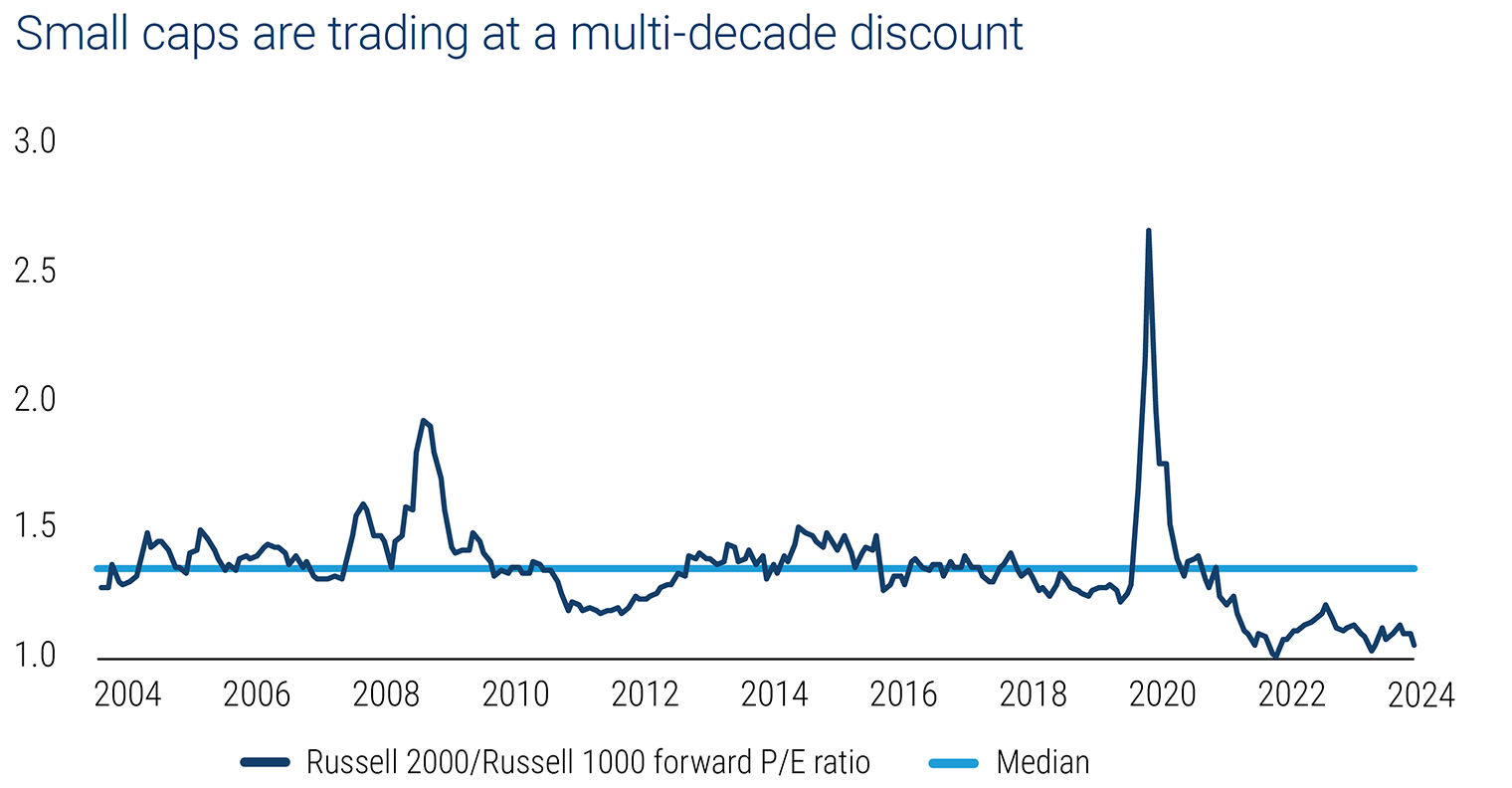

Another reason to believe in the staying power of the rotation to small caps is valuations. Historically, investors have paid higher multiples for small-cap growth potential. However, as large-cap tech performance and valuations have soared over the past several years, that equation has flipped. For some time now, smaller U.S. companies have been trading at a significant discount to large caps. Even with the recent shift in performance toward small caps since July, the asset class remains attractive — both in comparison to large caps and to historical norms.

Source: FactSet and Columbia Threadneedle Investments as of August 31, 2024. Small-cap stocks are represented by the Russell 2000 Index, large-cap stocks are represented by the Russell 1000 Index. An investment cannot be made in an index.

It’s important to remember that undervalued small caps have been reliable performers over the long term. For example, over the last 22 years, small-cap value has delivered an average total return of 8.1% per year, Of those 22 years, only seven were negative, and in half of the years, the asset class posted a total return greater than 10%.2

3. Access to a broader opportunity set

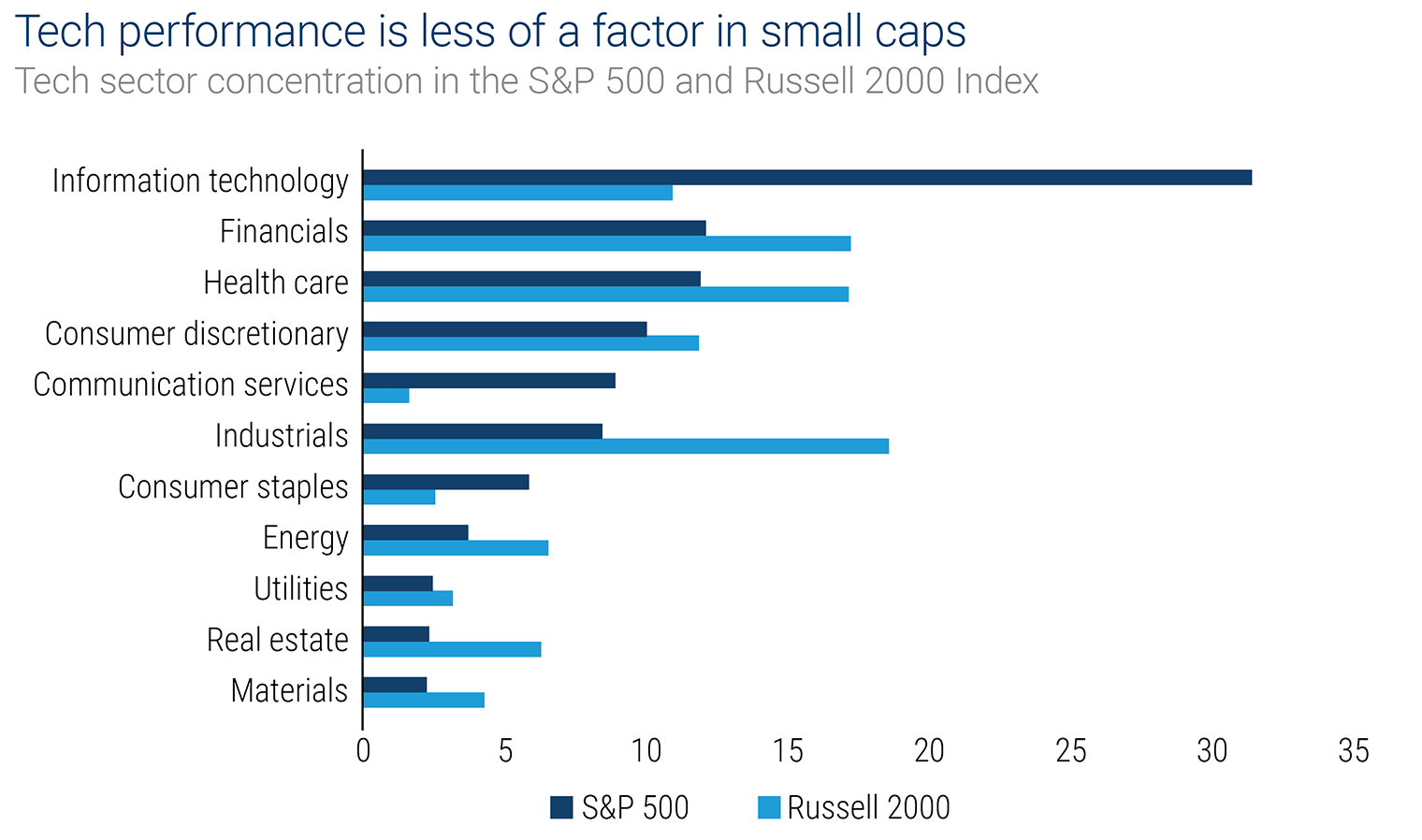

Small caps also offer exposure to a wider range of industries and sectors than large caps. As seen in the chart below, about 40% of the S&P 500’s weight is concentrated in just two sectors: information technology and communication services. In contrast, these same sectors account for only 12.5% of the Russell 2000’s total value. The dominance of these sectors, which has recently benefited large caps, may soon become a headwind — particularly as tech-related companies face increasing regulatory scrutiny, especially with the upcoming elections.

Source: FactSet, Columbia Threadneedle Investments as of August 31, 2024. An investment cannot be made in an index.

The universe of small caps is more diverse and less covered by research desks than large caps. With less information available, it’s more likely that small-cap stocks may be mispriced, and there also tends to be more dispersion in their performance and valuations. This creates more opportunities to identify potential outperformance on a company-by-company basis through research and active management.

Bottom line

We believe the current environment presents investors with an opportunity to reassess their small-cap positioning. Small-cap stocks stand to benefit from a strong and resilient U.S. economy. They are also attractively valued and offer broad exposure to sectors and industries beyond those that dominate large-cap indices.

1 FactSet. As of August 31, 2024.

2 Russell and Columbia Threadneedle Investments. As of August 31, 2024.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.