Thesis

International equities are interesting when considering the weak dollar narrative. While in the ETF space there are numerous alternatives, the closed-end fund segment contains fewer names. One of them is the Voya Emerging Markets High Dividend Equity Fund (IHD), a CEF we have not covered before.

In today’s article we are going to go through the fund structure, its holdings and analytics, as well as its performance.

What Does IHD Do?

Let us start with the CEF objective statement:

The Fund’s investment objective is total return through a combination of current income, capital gains and capital appreciation. The Fund invests primarily in dividend producing equity securities of issuers located in emerging markets.

The name is an active fund that uses a proprietary quant methodology to select underlying equities, while at the same time it employs a call writing strategy on the portfolio. We have seen the call writing strategy on a number of equity CEFs, but what is innovative here is that IHD writes call options on liquid EM ETFs rather than only the underlying holdings. Let us have a closer look at the analytics of the options and the rest of the holdings.

Holdings Parsing

The name is reminiscent of the iShares MSCI Emerging Markets ETF (EEM) via its geographic composition:

- China: 30%

- Taiwan: 19%

- India: 15%

- South Korea: 11%

- Brazil: 4%

- Saudi: 3.5%

- South Africa: 3%

- Other: residual

We have seen the same overweight China position in EEM, with the top 3 countries very similarly represented.

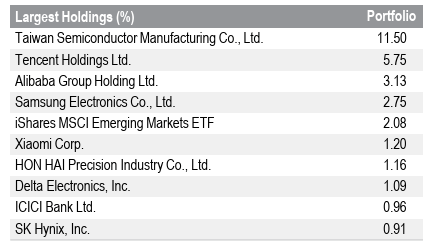

In terms of individual equities present in the portfolio, we have the following top 10 holdings:

Holdings (Fund Fact Sheet)

Taiwan Semiconductor represents the largest holding at 11.5%, followed by Tencent at 5.75% and Alibaba at 3%. There is a significant concentration of large cap technology stocks in this CEF. We can see the technology tilt for the CEF via its top sectors as well:

- Technology: 26%

- Financials: 21%

- Industrials: 10%

- Communication services: 9.8%

- Consumer discretionary: 9.4%

As we shall see further in the performance section, this composition was responsible for fairly muted results in 2024.

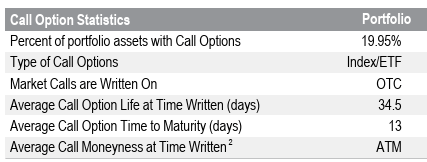

Let us now look at the options structure the fund employs as well:

Options (Fund Fact Sheet)

Roughly 20% of the portfolio is overlaid with call options, options that have a fairly short maturity of only 34 days at the time they are written. Given the laddered approach in the fund, the average call option time to maturity is only 13 days. The CEF writes calls at the money rather than leaving upside. We like this strategy for high-volatility names in the EM space.

Performance

Let us look at the CEF’s performance from two angles: firstly as a net yearly total return, and secondly as compared to EEM from a total return perspective.

Looking back a few years, we see the following total returns posted per year:

- 2019: +20%

- 2020: +1.9%

- 2021: +7.3%

- 2022: -17%

- 2023: +14%

- 2024: +6.6%

- 2025: +40%

- 2026: +3.6%

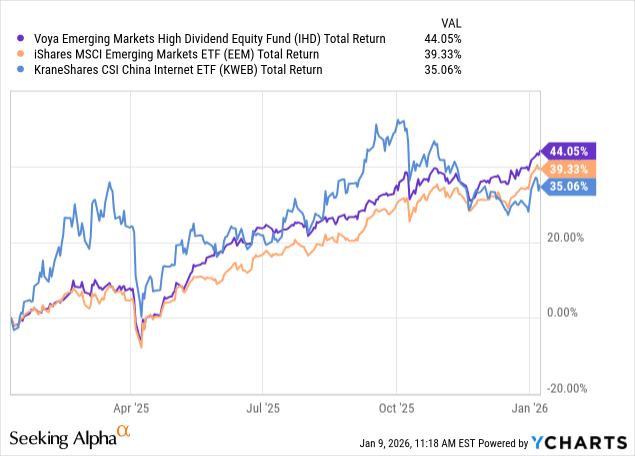

The fund had an absolutely astounding 2025, helped by the resurgence in China equities. From a relative value perspective, we can graph the name versus EEM:

We can clearly see the interdependency between the three names in the past year, with IHD and EEM posting very similar results, all while the KraneShares CSI China Internet ETF (KWEB) had a more volatile year and ended up lower than the two names.

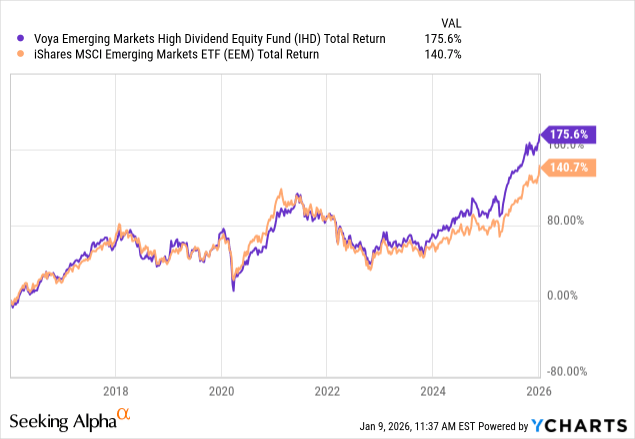

Longer term, EEM and IHD have similar return profiles:

The two funds had very similar total return profiles until recently, when IHD’s active security selection resulted in an outperformance. Investors should always prefer active funds over passive ones if the manager is good and is able to add alpha.

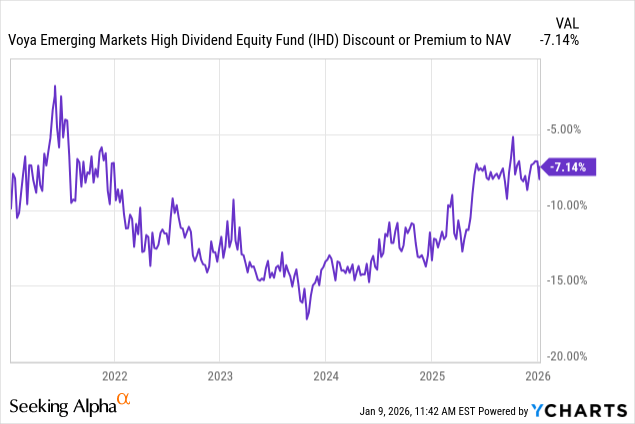

Premium/Discount to NAV

From a valuation standpoint, when considering the discount, the CEF is back to fair value:

We can see how the discount widened to -15% in 2024 when the name was posting poor results. Today the name is trading at a -7% discount to net asset value, a figure that is fair value considering the top of the range is -5%. As with any CEF, we tend to see this second-order risk metric move around with performances. Unless the name manages another astounding 2026, it is bound to give back 2-3 percentage points here and move to a -10% discount.

Do Not Ignore Geopolitical Risks

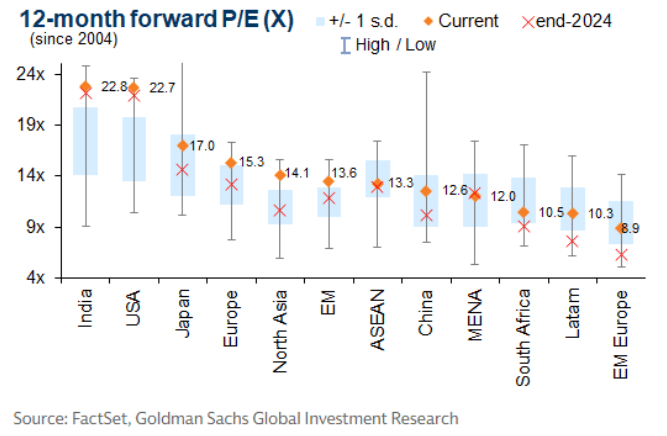

From a traditional P/E perspective, China is not overvalued yet:

Valuations (Goldman)

As we can see from the table above, China is not overvalued yet, but India is. So is EM overall. Nonetheless, for these jurisdictions, we can still see an expansion of P/E ratios during calm markets.

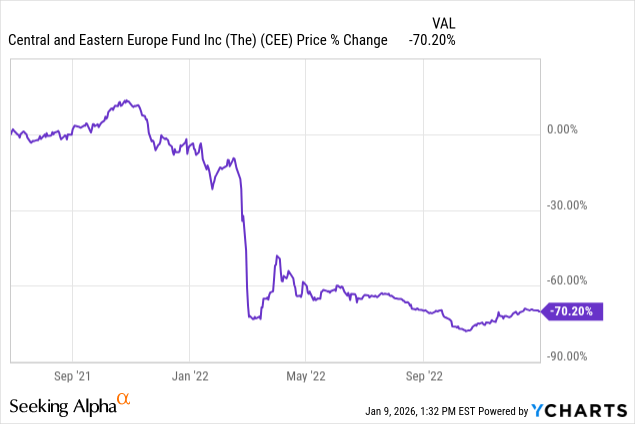

However, one of the biggest issues for us in terms of IHD is the geopolitical risk that comes with Chinese names. Investors should never forget the lesson learned when Russia invaded Ukraine. In a matter of weeks, all the Russian equities collapsed and got delisted from Western exchanges. There was a monumental wipeout of wealth there, and one can see that in the price action for The Central and Eastern Europe Fund, Inc. (CEE), which was long many Russian names:

We are living in a world where the former president of Venezuela was taken prisoner from his own country by the United States and where three world powers seem to play strategic chess. In January 2026, President Trump stated the following:

“He (Xi) considers it (Taiwan) to be a part of China, and that’s up to him what he’s going to be doing,” Trump told the newspaper on Wednesday.

The geopolitical forces at play show an active United States, which is setting the rules in North and South America whilst trying to get European powers to do more in terms of Russia. China seems to have the final say on Taiwan, and an invasion there could have very serious consequences for China equities.

Conclusion

IHD is an emerging markets CEF that historically has mirrored EEM. The CEF has outperformed its ETF peer in the past two years, thanks to active management and options use. We find the name fairly valued and are cognizant of geopolitical issues around its China holdings.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.