The Last Supper (of Software)

In a way, this year’s market movements are quite ironic. Everything has happened in these first (almost) two months. January was terrible, but February was “quietly” even worse.

We’ve repeated our “software is eating the world” mantra for the last 15 years as if it were some sort of religious dogma, and we’ve built valuation cathedrals based on price-to-sales multiples that would have made everyone pale during the tulip bubble. And we’ve ignored the obviousness of net profit margins while believing that 90 percent gross margins were sacrosanct. We’ve also rewarded companies that own absolutely nothing (I am prepared to provide you with a minimum of 50 to 100 company names) other than code lines, intellectual property, or promises about the future. On the other hand, we have penalized anyone who had the audacity to dirty their hands by dealing with atoms, factories, warehouses, or raw materials extraction.

Now, we stand before the ultimate paradox. The same technology that was supposed to guarantee the dominance of digital technology (Generative Artificial Intelligence) forever is instead proving to be a digital hourglass that is consuming its own offspring.

So, let me state clearly:

AI isn’t eating the physical world; AI is eating software.

Retail investors continue to look for their next “To the Moon” lottery ticket, while those commonly referred to as “smart money” have begun a silent but brutal hunt. It is no longer about hunting down the best potential investments; it has become the “hunt for losers”.

This is the era of the liquidation of the intangible, where the goal is not identifying companies that will grow, but avoiding companies that will be lost in the annals of time.

Anatomy of the Week

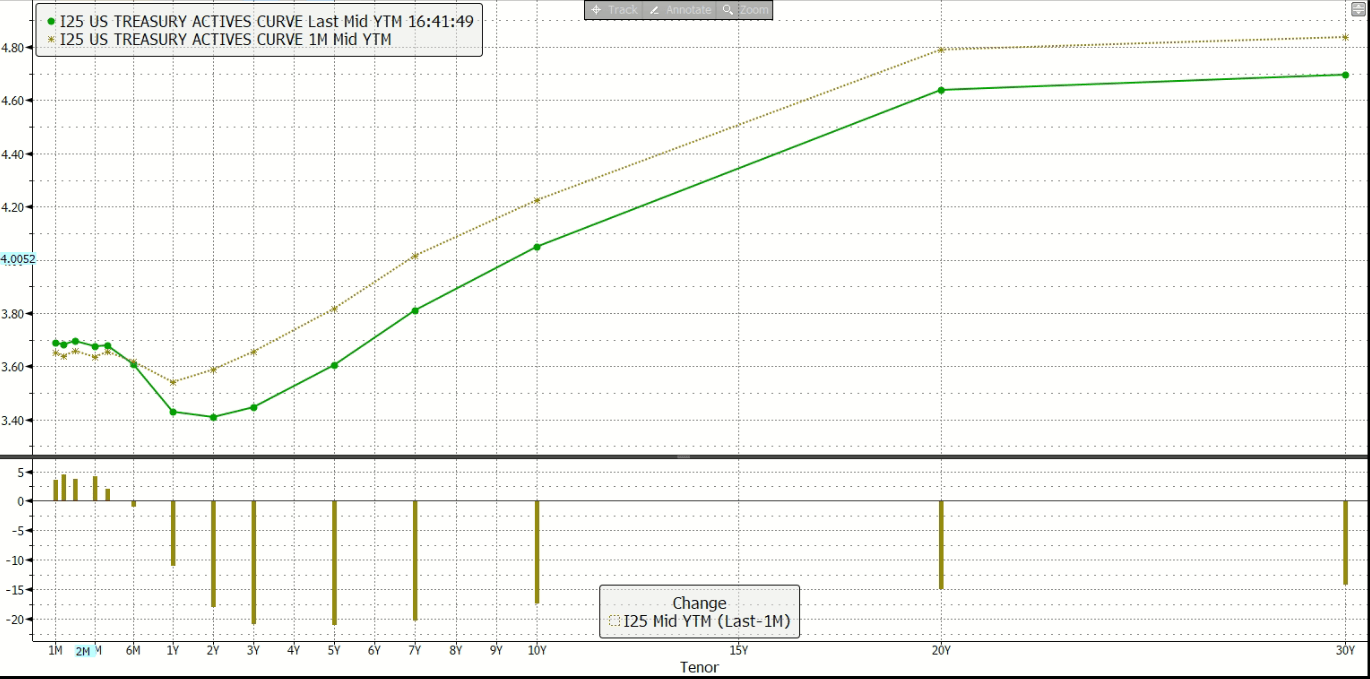

Last week was an example of economic balance between two views. On one hand, we saw the labor market reports showing a possible accommodative Fed and, therefore, possible rate cuts. However, that same week, we saw a stock market that showed extreme selectivity as the true hallmark of this phase.

Agar Capital, Bloomberg Terminal

Regardless, I do not think we are seeing blind panic or indiscriminate systemic risk-off. Instead, we have moved into a mature phase of the economic cycle, characterized by multiple compressions due to unsustainable levels of expectation and the surgical repricing of certain business models. On the macro side, we saw some interesting developments in the shape of the yield curve for the long term: following the higher yields of the previous few weeks, yields declined somewhat as consumers spent less money and the labor market reported less encouraging results than expected, and both pieces of information provided hope that the disinflationary path would continue and therefore provide the Federal Reserve with a more dovish stance. Nonetheless, in a typical hall of mirrors, a better-than-expected jobs report was released in parallel, and subsequently, there was little enthusiasm generated regarding the possibility of cuts being made. In fact, it is clear now that the data is no longer synchronized: the overall economy remains solid, but each of its component parts is undergoing a correction.

Agar Capital, Bloomberg Terminal

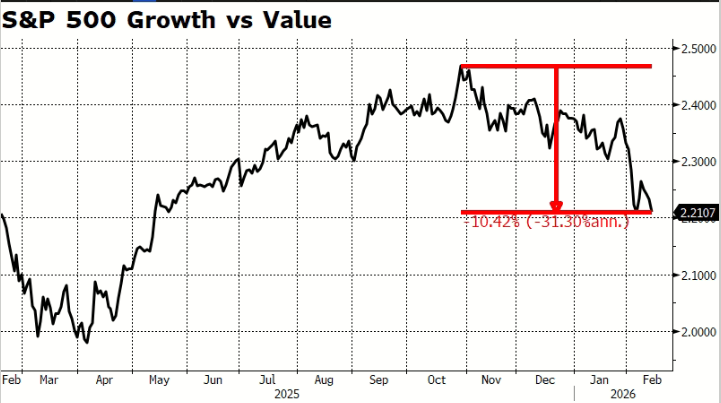

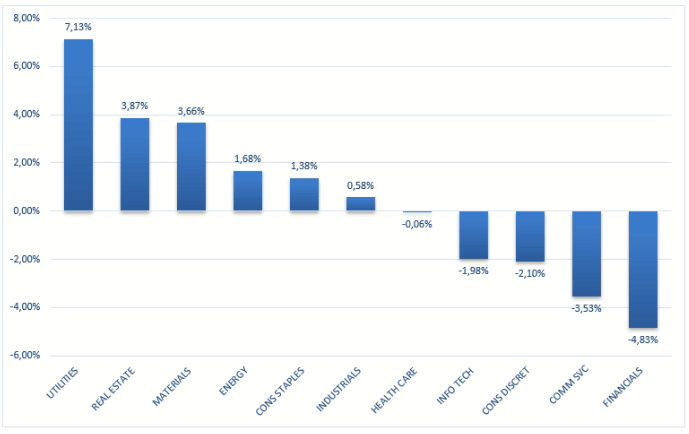

The weekly lead would look like a classic defensive rotation on the surface; utilities and real estate did well, while tech, telecommunications, and select financials underperformed. But looking at the decline through the lens of a traditional “growth to value” or “cyclical to defensive” rotation does not consider what I believe are significant changes in the nature of investing today.

Agar Capital, Bloomberg Terminal

Investing today is no longer about whether a company is a “growth” stock versus a “value” stock; today, investing is more fundamentally about “Can your business model be replaced by artificial intelligence?“

Agar Capital, Bloomberg Terminal

If a company’s business model could be diminished or disrupted by AI (similar to what has occurred recently for software-as-a-service (SaaS), logistics, data companies, etc.), then the price the investors are willing to pay for the terminal value of the company immediately declines. If the potential disruption by AI is minimal or the business is “physical“, then the valuation remains intact.

Goldman Sachs has made a comparison of various asset-light industries today to the publishing industry of the early 2000s. At one time, those industries were seemingly impervious to technological disruption until the internet changed everything and destroyed their ability to set prices. Today, many businesses involved in providing intermediary services such as brokerage or advisory services are being viewed with the same level of skepticism as was the publishing industry when it was first impacted by the internet.

While AI, WisdomTree Artificial Intelligence and Innov Fund ETF (WTAI), may be able to perform tasks such as writing code, automating processes, and replicating services, AI cannot transform itself into an electrical grid, nor can it replace a physical asset or logistical infrastructure.

Therefore, the rotation that is occurring today is not simply “growth versus value”; rather, it is “potentially destructive versus less destructive”. Over the last two years, the story has been who wins at AI; today, the story is far more ominous, and the question is, “Which model is most at risk of becoming commoditized?” When the focus of the market shifts from selecting the winner to identifying the loser, the selection process can be very brutal.

The ETF Trap and Flow Mechanics

Technically speaking, there has been a factor to help increase the intensity of the movement to the point of being chaotic and unpredictable. Those in the sector know these types of moves extremely well, as they now make up what we would call the backbone of the new and evolving passive and ETF (exchange-traded fund) flow-driven market.

ETFs have become popular as a way to create portfolio diversification with ease while also increasing accessibility to the markets. Personally, I also use (to a limited extent) ETFs as a tool to gain diversified exposure in sectors and/or geographical areas where it is difficult for me to expose myself (for example, the Indian market, Korea, etc.).

Regardless, I believe that in certain instances, ETFs can make the market more complicated than necessary. More specifically, when trend reversals occur, what was once their biggest advantage (the ability to provide diversified exposure) becomes their worst liability (distortion multiplier). When an investor fearing the impact of an “AI bubble” clicks the “sell” button on a tech ETF, the algorithm then goes out and sells the entire basket of stocks contained therein.

As a result of this action, we see a phenomenon known as the “basket effect”, which liquidates both companies with fragile or asset-light business models and companies with high margins, true cash flow, and irreplaceable physical assets that just happen to be in the same sector code as the latter. It is a purely mechanical process; it is a blind sell-off. Also, the speed of the algorithms used in algorithmic trading causes repricing to occur rapidly and in an irrational manner.

When panic occurs, there are many who will capitalize on the new opportunity. The extreme price asymmetry generated during these times provides the greatest potential for the investor with a longer-term perspective. I believe that physical AI (the type created with cables, power, and hardware) has an extremely strong structural demand that can be seen from all-time high orders and backlogs for physical AI products. If there were still some questions in anyone’s mind, AI is changing how industrial supply chain systems operate.

A major economic downturn is not required to bring down stock prices when multiple factors (valuation multiples and expectations) have reached extreme levels; only a paradigm shift in how investors perceive risk is necessary. The standard has been raised today: investors who provide the creation of genuine value using technology will be rewarded, while those at risk for technological devaluation will be mercilessly reevaluated.

Capex Break?

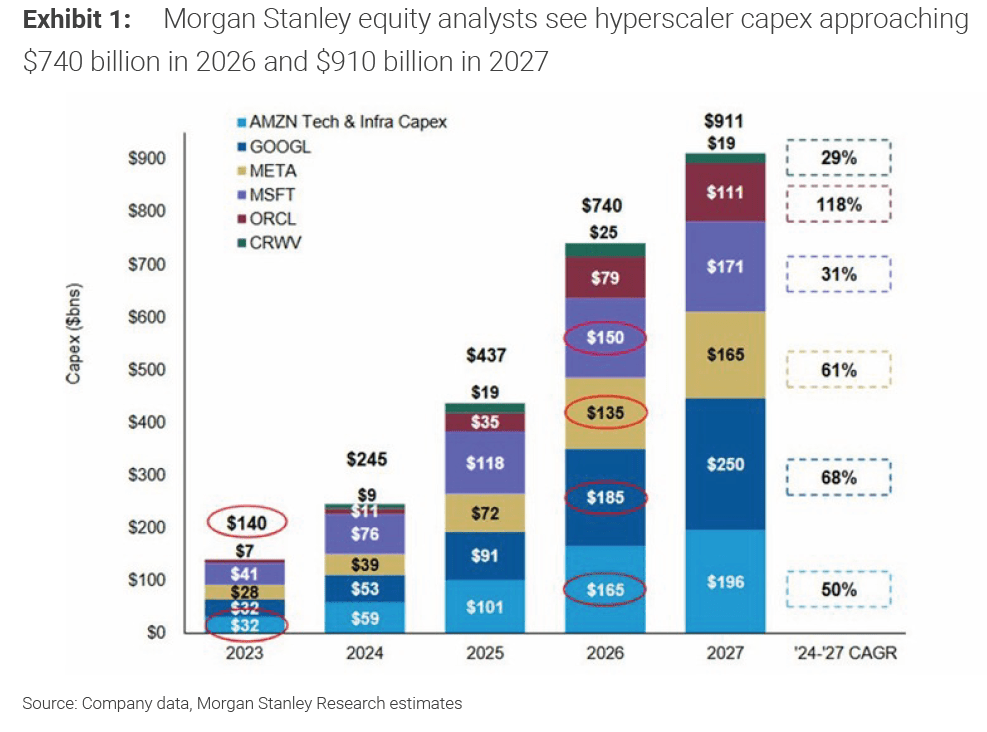

We appear to have a near-perfect curve in terms of the megacap investments into AI.

Morgan Stanley

I wondered, therefore, the day that one of these companies finally decides to go ahead and say, “Let’s back off a bit,” how do you think the rest of the market would respond?

I’m not trying to be pessimistic or anything else; I simply wish to apply the normal industrial logic to this type of situation. Eventually, an aggressive push like this will absorb and optimize. The result will be understanding what actually works and what does not. This is a highly unstable market today, with the majority of the instability caused by the hype surrounding AI. It is reasonable to assume that at some point, the market will declare a slowdown in investment digestion.

Firstly, the semiconductor space (especially memory) probably gets hit the hardest by a pullback in investment. Memory is the most cyclical and most vulnerable to fluctuations in demand. So, if a megacap were to decide to reduce spending in the semiconductor area, stock prices such as Micron Technology, Inc. (MU) could experience a severe price decline similar to what was seen in silver a few weeks ago: when the money stops flowing, it happens fast.

However, be cautious because this is not always a bearish sign for the whole market. In fact, a reduction in capital expenditures may help stabilize the Mag 7. Lower CapEx results in lower pressure on cash flows, less need for financing, and therefore, less worry about “who spends the most“. Additionally, a period of consolidation can be viewed as discipline, not weakness.

And then there is the software side. If most investors are currently long on AI infrastructure and short on legacy software due to their current trade positions, a pullback in CapEx would likely cause them to reevaluate those positions. What is left is degrossing, hedging, and massive short squeezes in the severely beaten-down names. In these instances, technical movements can be extreme.

Market Structure

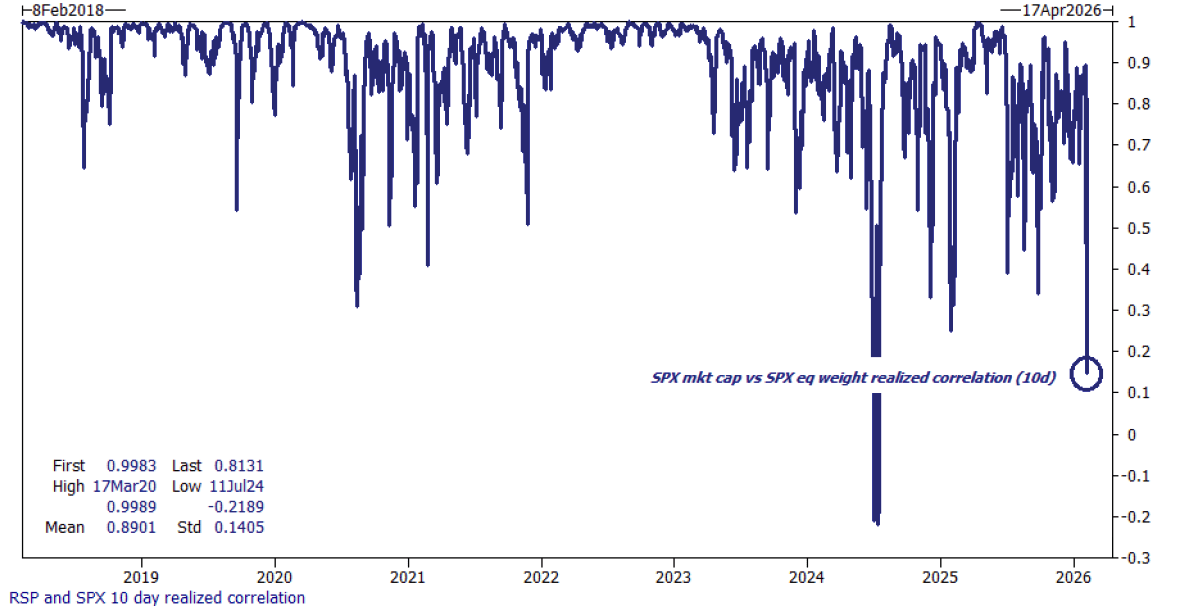

At first glance, all appears well with the S&P 500. The S&P 500 has held its own, volatility is still relatively low, and the VIX does not appear to be signaling panic. However, this is an optical illusion.

The chart I am providing today provides the ten-day correlation between the S&P 500 market-cap weighted (the Big Tech-dominated version) and the S&P 500 equally weighted (the ‘average’ economy, the other 493 stocks).

Goldman Sachs

For many years, these two correlated very closely, but from 2015 through 2024, the average correlation was approximately 0.89. Essentially, everything went up together, or everything went down together. This is no longer the case. Today, we are below 0.20, which is effectively a vertical decline in correlation.

Therefore, it is possible for the seven largest stocks to move in one direction, while the remaining 493 stocks move in the opposite direction. A dispersion-driven market is no longer a beta-driven market.

When correlation breaks down, two things occur:

- Stock selection is critical.

- Mistakes are paid for at a much greater cost.

No longer can investors simply buy the S&P 500 and wait. Investors must decide on which side of the fence to be on.

Be Resilient, Not Just “Growth”

We should avoid being misled into thinking that, since the indices seem calm right now and we believe that AI is going to change everything, we won’t see anything out of the ordinary. Yes, AI will change everything. However, when it does, it will force those on the fringes who are trying to sell something that can be replicated through algorithms in a matter of months back onto their heels (we saw that happen just recently).

It’s the law of nature—survival of the fittest. As we move forward over the next few months, our strategies need to be far more targeted than they have ever been before. I’ll give you my suggestions:

- Don’t get caught up in the hype: when the product is replaceable by cheap alternatives or can be easily recreated using AI internally, the company is at risk of losing the pricing power.

- Take advantage of the “basket” effect during volatile sell-offs: ETFs tend to throw everything together during these times and don’t discriminate. Therefore, opportunities come from quality industrial, infrastructure, and energy companies. With both liquidity and patience, you can select during these times.

- Prepare for capex volatility: when/if there is actually a slowdown in AI investments, the shock will be fast. First, it will impact those who rely on marginal demand (such as memory and cyclical parts), and then it will spread. But the shock will also help to better price structural winners, such as physical infrastructure, energy, and critical supply chain companies.

This phase of the market cycle is no longer growth vs. value. It is resilience vs. replicability. The hunt for the loser has already begun.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.