Introduction & Investment Thesis

Reddit (RDDT) stock was in the red yesterday, down 5.5% after Google (GOOG) announced a broad overhaul of Search at its I/O 2026 developer conference, which investors fear could lead to a decline in user traffic flow and monetization for Reddit.

As an existing investor in Reddit for The Pragmatic Optimist Portfolio, I believe the potential Google-related headwinds are already priced in, as the stock carries a significantly higher risk premium compared to, say, Meta (META). I say this because both stocks are trading at a similar forward P/E ratio, even though Reddit is expected to grow its revenue and earnings by twice and thrice the rate of Meta, respectively, over the next three years.

While Google-related risks are not negligible, the good thing is that Reddit’s management has already been doubling down on their own AI-powered search platform, which is seeing strong momentum in user growth and monetization, with its Q1 FY26 earnings beating estimates on both the top and bottom lines.

Not only that, the majority of users who come to Reddit from Google Search tend to be “logged-out” users that carry far lower ARPUs (Average Revenue Per User), meaning that even if user traffic flow to Reddit drops as a result of Google’s Search updates, its monetization engine should be shielded.

As a result, I believe that the selloff in Reddit is actually a gift in disguise, where I would use the opportunity to expand my position in the company while reiterating my “buy” rating on the stock.

Why Do Google’s Search Updates Matter to Reddit?

Google announced a broad overhaul of Search at its I/O 2026 developer conference, where the company introduced an AI-powered multimodal search interface and agentic AI capabilities for a more interactive and personalized user experience.

In response, Reddit’s stock came under pressure yesterday as investors grew concerned about the risk that the company could now face, as users could just find the answers to their queries directly through Google’s AI Overview, without the need to navigate away from the search page. This would then lead to Reddit losing the number of outbound organic clicks and DAUq (quarterly average of Daily Active Uniques), as well as the opportunity to convert the guest into a registered “logged-in” user, even though a Reddit thread may have been the foundational data source for Google’s AI answer in the first place, thus threatening Reddit’s traffic monetization model.

The reason why investors are particularly worried is that Google Search drives roughly 40-50% of Reddit’s total incoming user traffic. While Google pays Reddit a flat data licensing fee of $60M, the former likely has an asymmetric monetization advantage over the latter as users stay locked inside the Google ecosystem.

However, here is the thing.

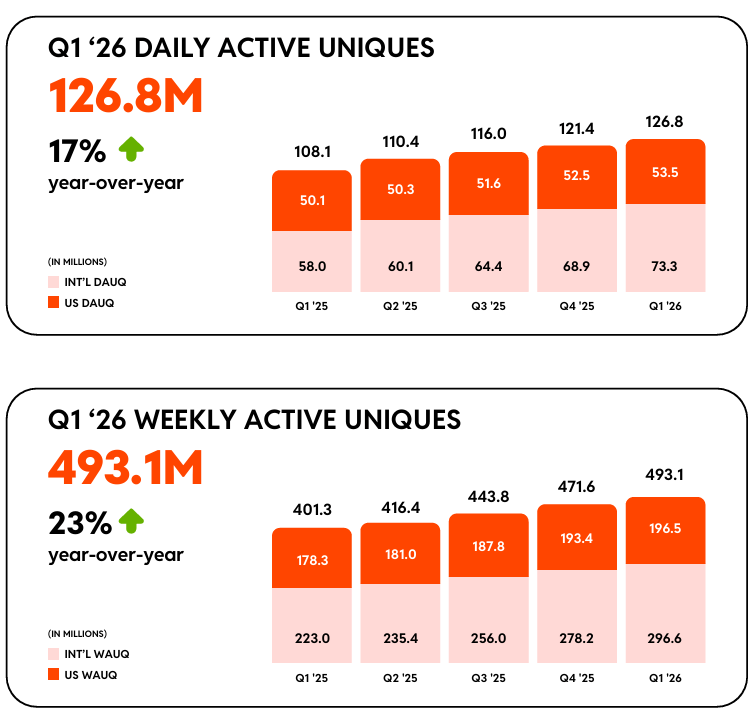

Reddit’s management already knows the extent of its platform’s vulnerability to Google Search and, as a result, has been strategically building its own defenses by transforming its platform into an AI-powered search destination with the broad rollout of Reddit Answers. We can see that translating into strong engagement growth, with both DAUq and WAU (Weekly Active Uniques) growing 17% and 23% YoY in Q1 FY26 to 126.8M and 493.1M users, respectively.

Q1 FY26 Shareholder Letter: Strong momentum in user growth for Reddit

What is also driving strength in traffic growth is the company’s efforts in scaling internationally, where its content is translated into over 30 languages and optimized to deliver high-quality and locally relevant content to users across the world.

Plus, what is important to note is that a massive portion of the traffic that comes through Google Search are “logged-out” users, who carry far lower ARPU than that of a registered logged-in app user, as the latter spend a lot more time on the app and see more ad impressions. In other words, even if Reddit actually sees its overall user traffic drop as a result of the updates made to Google Search, its monetization engine won’t be meaningfully impacted.

Having said that, I am not saying that the Google headwind is negligible. However, Reddit’s stock already carries a higher risk premium to compensate investors for the underlying risk, even though its monetization engine is on fire.

Reddit’s Ad Monetization Engine Is On Fire

In the latest Q1 FY26 earnings, Reddit’s advertising revenue grew 74% YoY, contributing over 94% to its total revenue, which also grew at almost a similar rate to the previous quarter at 69%, beating estimates by 8.79%. This is the case, as both ad impressions and ad pricing grew in unison this quarter, demonstrating that the system is getting better at allocating attention to higher-value placements.

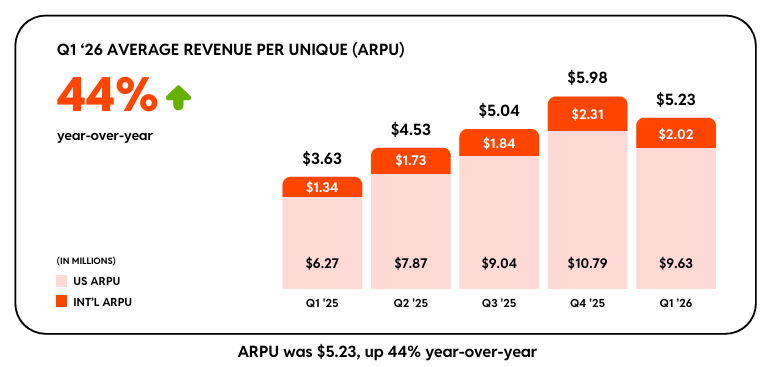

This is also reflected in ARPU, which grew 44% on a YoY basis, with U.S. ARPU growing at a faster rate than international ARPU and contributing to the bulk of the revenue, as can be seen below.

Q1 FY26 Shareholder Letter: ARPU expanding on a YoY basis for both US and International geographies

As management discussed in the shareholder letter, they have built their ads business on “context, interest, and commercial intent,” and when you combine an engaged user base with commercial intent, it creates a powerful environment for advertisers, who increasingly allocate a higher amount of their budget on the platform for superior return.

During the quarter, Reddit saw growing adoption of their Reddit Max campaigns and Dynamic Product Ads that are designed to optimize lower funnel objectives, with advertisers seeing significantly higher conversions and lower cost per acquisition.

The Risk-Reward Continues To Be Highly Attractive

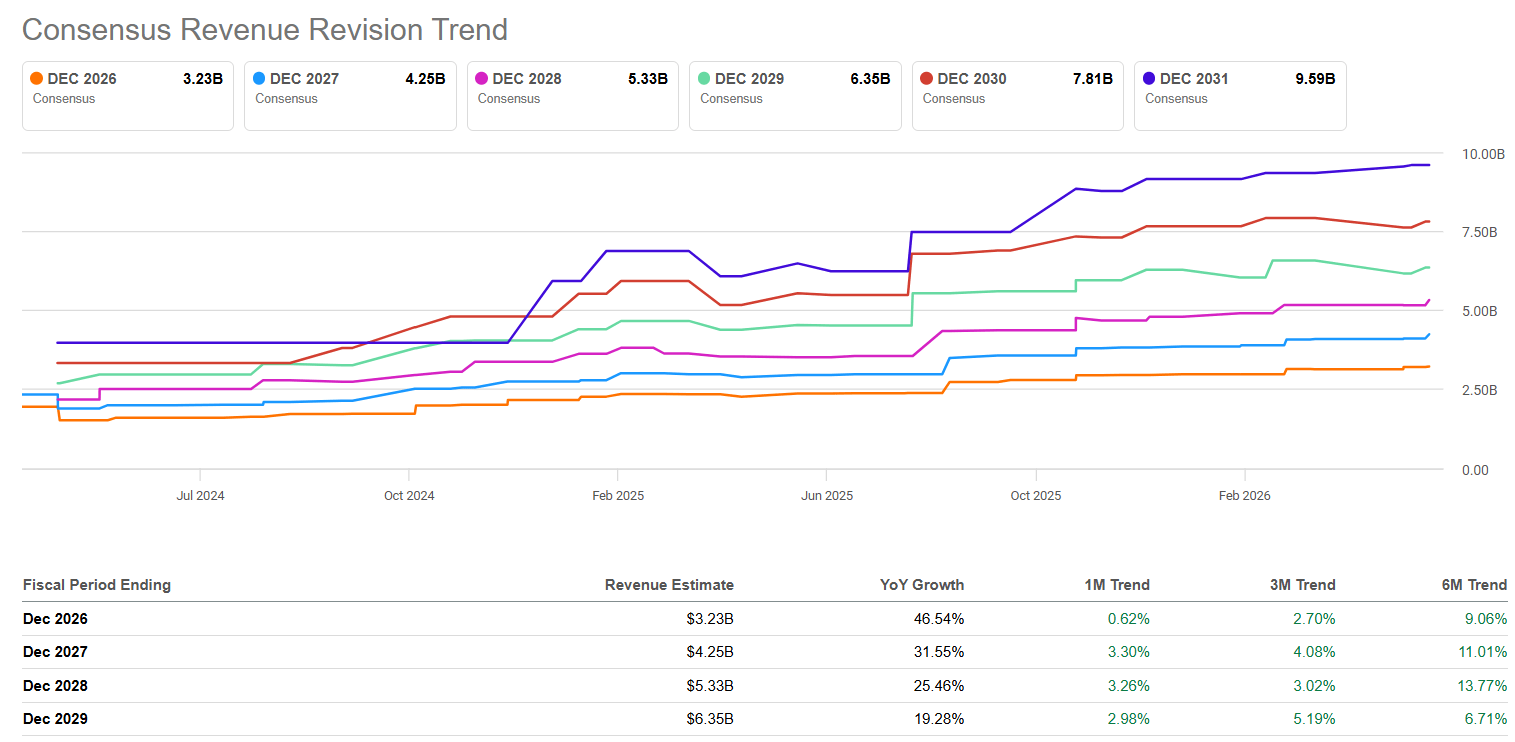

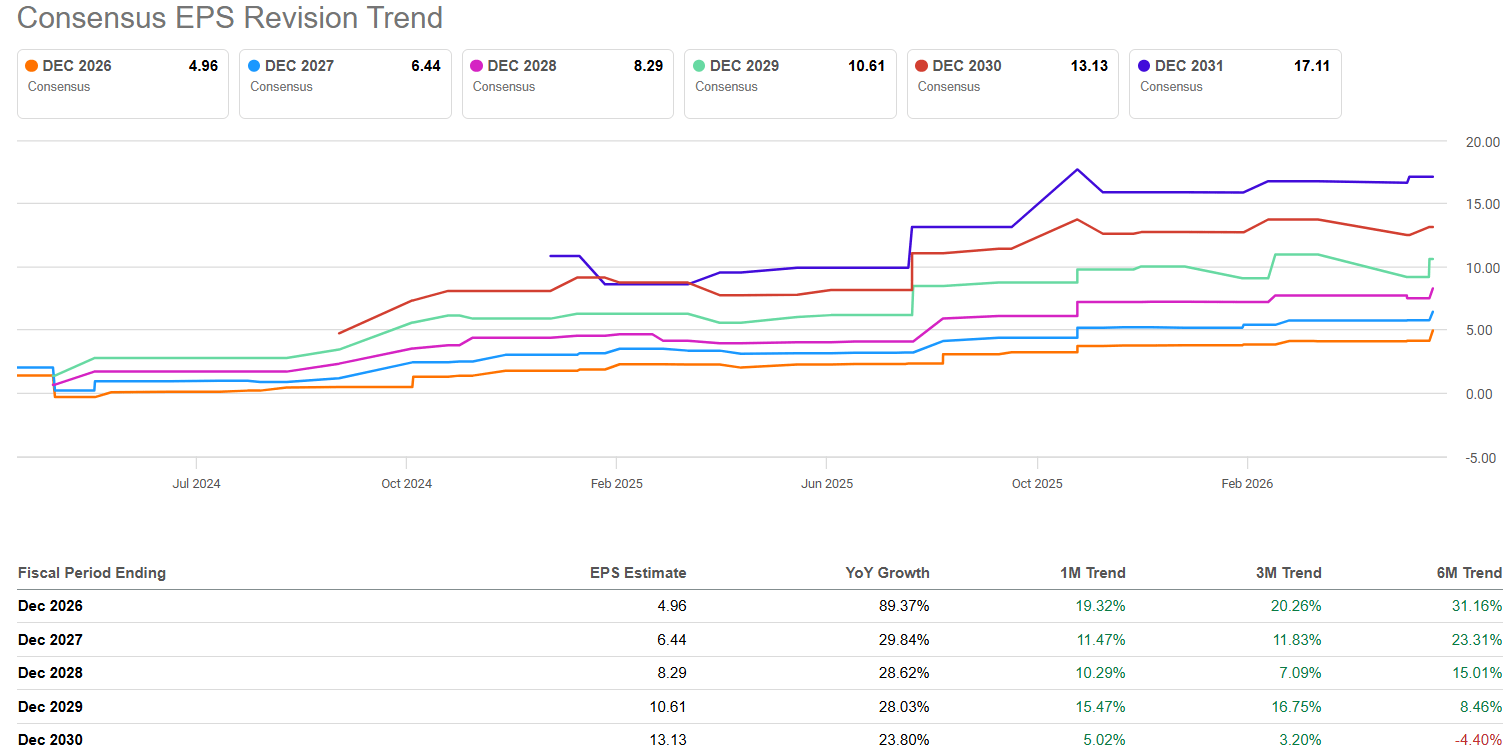

The good news is that Reddit has received a significant volume of upward revisions to both its forward revenue and earnings growth estimates by consensus, which is very encouraging in my opinion.

On the revenue front, the company is now expected to grow its top line by 46.54% YoY in FY26, which will be followed by 31.55% and 25.46% over the next two years to roughly $5.33B by FY28. Note that these revenue estimates are being revised higher over the last one, three, and 56 months.

SA: Upward revisions to Reddit’s forward revenue growth estimates by consensus

Meanwhile, when it comes to profitability, its superior monetization engine is enabling it to expand operating leverage, with both its gross and adjusted EBITDA margins expanding on a year-over-year basis. Meanwhile, when it comes to its earnings per share estimates, analysts have been heavily revising them higher, as can be seen below.

SA: Strong upward revisions to earnings per share estimates by consensus

Reddit stock currently trades at a forward non-GAAP P/E ratio of 20.91x based on an earnings per share growth estimate of 89.37% YoY. In fact, its forward P/E ratio collapses to just 17x when taking its FY28 earnings per share of $8.29 into account.

Meanwhile, Meta, which is projected to grow its earnings per share by 9% YoY in FY26, is trading at a forward P/E ratio of 19.00x. This just goes to show how large a risk premium Reddit is already carrying, trading at a similar forward P/E ratio as Meta, even though it is projected to grow its revenues and earnings at twice and thrice the rate, respectively, over the next three years.

However, I do believe that given where the stock is currently trading at, Reddit offers extremely attractive risk-reward. Based on Wall Street price targets, the stock has a potential 53% upside to the “average” price target of $225 per share, compared to the 17.8% downside risk to the “low” price target of $120 per share.

Risks and Conclusions

There is no doubt that the risk-reward is quite attractive at current levels.

Having said that, the stock may be subject to volatility from investor sentiment surrounding the Google headwind and how it impacts Reddit’s user traffic and monetization.

But like I said, Reddit has been building its own AI-powered search with strong momentum in its ad monetization engine. Plus, the stock already carries a high-risk premium that I believe sufficiently compensates investors for the underlying risks.

I am currently invested in Reddit at a “starter” size for The Pragmatic Optimist Portfolio, and I will look to expand my position size at current levels. Having said that, a break below its March lows will be relatively problematic, as the stock would then likely head to the $80 levels based on my technical analysis.

However, I don’t believe that would break my bullish long-term thesis; however, in the short term, I will be careful with my position sizing in the company for my portfolio.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.