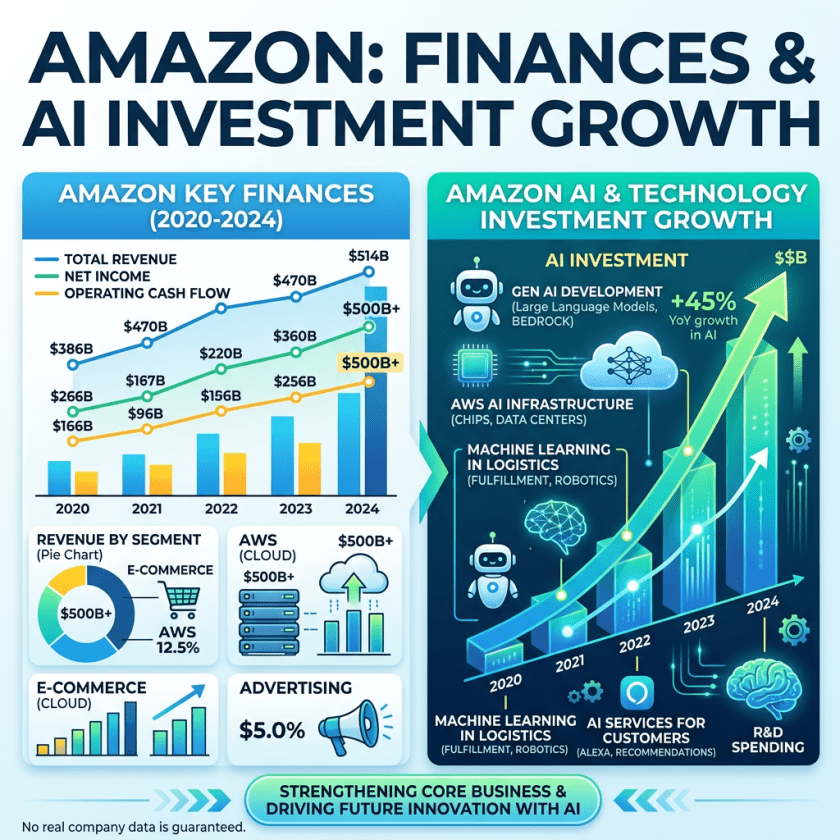

Amazon’s (AMZN) investment case is becoming more controversial because free cash flow has collapsed while capital expenditures are rising sharply. In Q1 2026, trailing-twelve-month free cash flow fell to $1.2 billion from $25.9 billion a year earlier. The reason was not operating weakness. Actually, operating cash flow increased 30% to $148.5 billion. The issue was a $59.3 billion YoY increase in purchases of property and equipment, primarily driven by AI infrastructure investment. On a strict basis, also netting out stock-based compensation, TTM free cash flow is running close to negative $22 billion.

That distinction is the investment case. Amazon is not seeing cash flow deteriorate because the business is weakening. It is converting operating cash flow into infrastructure, specifically related to AI. The key question is whether this capex earns attractive returns. My view is that it likely does, because the spending is attached to clear demand signals: AWS is accelerating, AI revenue is already material, Amazon’s custom silicon business is scaling rapidly, advertising is growing above 20%, and retail unit growth is improving.

AWS Is The Main Evidence That Capex Is Productive

In my view, AWS is the most important variable when looking at Amazon shares. And the read is supportive: In 2025, AWS revenue increased 20% to $128.7 billion. AWS operating income was $45.6 billion, implying a segment operating margin of roughly 35%. In Q1 2026, AWS revenue grew 28% to $37.6 billion, its fastest growth in 15 quarters. While AWS operating income jumped to $14.2 billion, implying a margin close to 38%. AWS AI revenue reached a $15 billion run-rate, which is roughly 10% of annualized AWS revenue.

In other words, Amazon is increasing infrastructure spending while its highest-return segment is accelerating on topline on a very large base, while operating margin is expanding. That is materially different from a company spending capex to defend a declining asset.

Custom Silicon Improves The Return Profile

The second part of the thesis is custom silicon. Amazon’s Graviton, Trainium, and Nitro chips are already above a $20 billion annual revenue run-rate and growing triple digits. Andy Jassy also said in the Q1 earnings call that the chip business saw nearly 40% QoQ growth in Q1, and would be closer to ~$50B if treated like a standalone chip company selling chips to AWS and third parties.

Amazon has already announced major AI infrastructure commitments: OpenAI consuming ~2GW of Trainium capacity from 2027, Anthropic securing up to 5GW of Trainium, 2.1+ million AI chips landed in the past 12 months, and 1+ million NVIDIA GPUs to be deployed starting in 2026. Amazon also says it now has over $225 billion of Trainium revenue commitments.

Custom silicon matters because the biggest risk in AI infrastructure is input-cost inflation, as hyperscalers are competing for limited supply. If everyone buys the same inputs at inflated prices, returns can compress. Amazon’s custom silicon reduces that risk. Graviton lowers general compute cost. Trainium targets AI training and inference. Nitro improves virtualization, networking, and security. Together, these chips give Amazon more control over AWS unit economics. In AI, cost per unit of compute is a strategic variable. If Amazon controls more of that cost curve, AWS can both price aggressively and protect margins.

Advertising Is The Retail Margin Reset…

Historically, Amazon retail looked structurally low margin because fulfillment is expensive. But that view misses the monetization layer on top of retail traffic. Every additional retail unit creates more search behavior, and thus more ad inventory. Retail scale therefore does not only generate retail gross profit. It also creates high-margin advertising revenue. Meta and Google largely monetize attention. Amazon monetizes consumers close to purchase. That makes the ad inventory more measurable and more directly connected to seller revenue.

With that said, I am very bullish on Amazon’s advertising business, which is now above a $70 billion trailing revenue run-rate and grew 24% YoY in Q1 2026. This is now one of the most important profit pools in the company. This is already visible in segment results. North America operating income increased to $29.6 billion in 2025 from $25.0 billion in 2024. International operating income increased to $4.7 billion from $3.8 billion.

… Which Gets Accelerated By Retail Consumption Growth

The second leg of the non-AI thesis is that the advertising flywheel becomes stronger as Amazon’s retail consumption grows. Higher purchase frequency increases search frequency, which in turn creates more monetizable ad inventory. So logistics investment that initially looks like a cost burden can later become an advertising accelerator.

That is why same-day and overnight delivery matter strategically. They make Amazon more habitual. The more habitual Amazon becomes, the more often consumers start their buying journey there. And once consumers start their buying journey on Amazon, sellers have no choice but to compete for visibility inside the platform. This creates a powerful margin loop, and, in my view, is one of the cleanest reasons to be bullish on Amazon. The retail business is becoming structurally different from what it looked like ten years ago.

Where Amazon Could Be In 2030

A reasonable base case is AWS revenue growing from $128.7 billion in 2025 to roughly $300-320 billion by 2030. That implies an 18-20% CAGR and is well below what consensus is projecting. I do think consensus ~$360 billion is possible. I just want to be conservative here, as projection of 2+ years is inherently speculative.

Refinitiv

If AWS margins remain in the low-to-mid 30s, AWS operating income could reach roughly $100-115 billion. Again, stable margins are conservative, judging on the latest trend.

For the rest of Amazon, operating income of $55-65 billion by 2030 looks plausible. The drivers are advertising growth, North America margin expansion, International scale, and logistics efficiency. Advertising alone could plausibly double over the period if it continues to grow meaningfully faster than retail revenue, I argue.

This implies potential 2030 operating income of roughly $155-180 billion. After tax, that could translate into approximately $125-135 billion of earnings power. At a market value around $2.7 trillion, Amazon is not optically cheap. But on $125-135 billion of potential 2030 earnings power, the stock trades at roughly 20-21x future earnings, with notable upside as my numbers are clearly on the conservative side. For a business with AWS, advertising, Prime, custom silicon, retail scale, and AI infrastructure exposure, that is attractive, especially considering that Amazon has historical never traded that cheap on earnings.

Seeking Alpha

A Few Thoughts On Risks

Memory and storage component cost inflation (Amazon flagged this directly this quarter) is squeezing server economics industry-wide, independent of which compute chip wins, and is worth watching alongside the broader NAND/DRAM pricing cycle.

Secondly, AI-related bookings are concentrated in a small number of very large customers (Anthropic, OpenAI, and Meta among them), so a slowdown at any one of them would show up quickly in AWS backlog growth.

Thirdly, Azure’s and Google’s own silicon programs will narrow Amazon’s cost-per-flop advantage over time, even if they don’t close it soon. And the FTC matter above is a real, if probably manageable, distraction specifically for the advertising segment.

Investor Takeaway

Amazon’s free cash flow has collapsed because the company is investing aggressively. But that may exactly be why Amazon stock is a Buy, as the market may be over-penalizing near-term free cash flow weakness and underweighting the operating income Amazon may be building.

The evidence is quite consistent. AWS is accelerating at the same time capex is rising. AI revenue is already material. Custom silicon improves the AI infrastructure return profile. Retail unit growth creates more transaction frequency. More transaction frequency creates more advertising inventory. Advertising improves retail margins. For investors willing to look through the capex cycle, that is quite a coherent bull thesis, in my view.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.