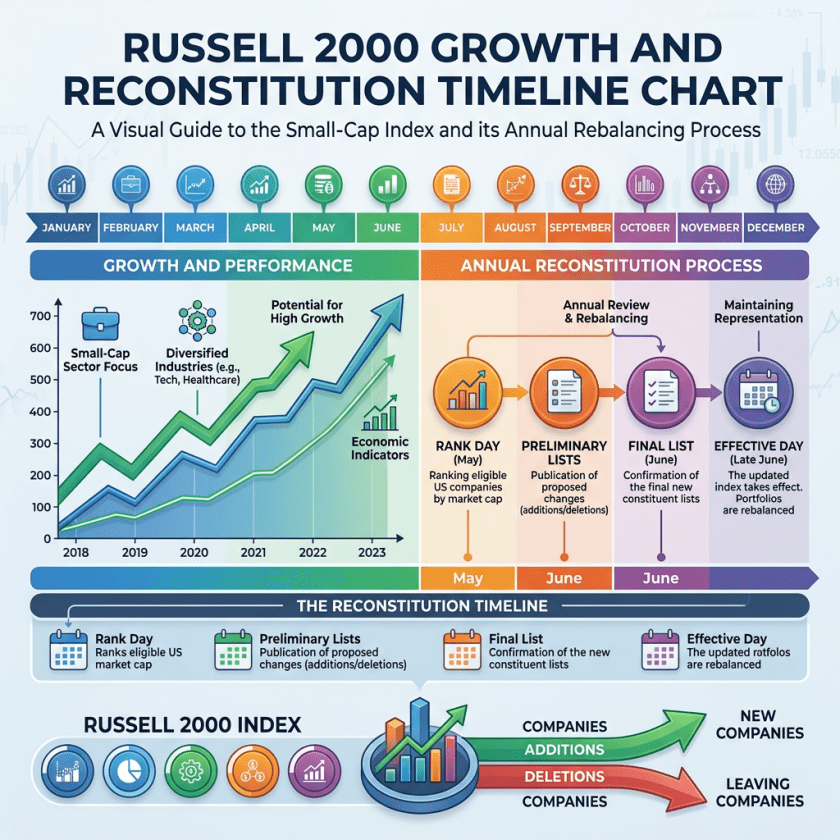

A New Reconstitution Calendar Takes Effect

For more than four decades, the Russell 2000 Index was reconstituted once per year, in June, as FTSE Russell identified which companies belonged in the small-cap benchmark based on their market capitalizations at the end of a May rank day.

Beginning with the June 2026 rebalance, that framework changed. FTSE Russell shifted to a semi-annual schedule, with reconstitutions in June and December, reflecting a judgment that annual reviews had become insufficient to keep up with the pace of capital formation and corporate restructuring in the modern equity market.(1)

The practical effect is meaningful. Under an annual schedule, companies that grew past the large-cap threshold could remain in the Russell 2000 for up to 12 months, distorting the benchmark’s representation of genuine small-cap dynamics.

Semi-annual updates reduce that lag, producing a tighter and more current portrait of where smaller domestic businesses actually stand. The June 2026 reconstitution, which takes effect at the U.S. market close on June 26, also introduces a larger retention band to reduce unnecessary turnover – a design improvement intended to lower transaction costs for funds tracking the index.

Market Capitalization Breakpoints Jumped 24 Percent

The data emerging from the preliminary June 2026 reconstitution lists tell a striking story about how much the U.S. equity market has grown. The market capitalization threshold dividing the large-cap Russell 1000 from the small-cap Russell 2000 rose 24 percent, from 4.6 billion dollars in 2025 to 5.7 billion dollars in 2026.(2)

The smallest company eligible for the Russell 2000 had a market cap of approximately 146 million dollars, up nearly 23 percent from the prior year.(3) Total Russell 3000 market capitalization increased 29 percent, from 58.4 trillion dollars to 75.6 trillion dollars.

These numbers reflect genuine wealth creation across market segments, not merely a narrow advance by mega-cap technology names. The total market capitalization of the Russell 2000 itself grew from 2.7 trillion dollars to 3.5 trillion dollars during the 12 months ending on rank day, a 30 percent increase that outpaced the broader index. That outperformance represents a sustained broadening of the equity rally that many market participants had anticipated but questioned throughout much of 2024 and 2025.

Earnings Growth Expectations Underpin the All-Time High

The Russell 2000 reached all-time highs in the week ending June 20, 2026, a milestone that coincided with building earnings momentum rather than pure multiple expansion.(4)

Bottom-up consensus estimates compiled through Bloomberg showed the Russell 2000 poised to deliver approximately 43 percent year-over-year earnings growth over the coming 12 months, roughly four times the 11 percent growth projected for the S&P 500 over the same period.(5)

Calendar-year 2026 EPS estimates for the small-cap index stood at approximately $102.56 per share as of June 1, representing growth of 17.8 percent over 2025.(6)

The sectoral composition of Russell 2000 additions in the June reconstitution reinforces the earnings story. Health care leads new additions, followed by technology, industrials, and consumer discretionary – four sectors where domestic orientation provides some insulation from trade-related cost pressures and where AI-adjacent demand is beginning to surface in smaller companies.(7) The 237 new additions include 17 recent IPOs, a sign that primary capital formation is again healthy enough to replenish the small-cap universe at scale.

What the Semi-Annual Shift Means for Active Managers

For active investors in the small-cap space, the move to semi-annual reconstitution changes the dynamics of the traditional June reconstitution trade. Index rebalancing has historically generated predictable price pressure in stocks near the Russell 1000/2000 boundary around rank day, as passive funds must buy additions and sell deletions simultaneously.

With a second rebalance now scheduled for December, the total June turnover should be lower – reducing the magnitude of the near-rank-day distortions that active managers have historically exploited.

At the same time, the broader structural picture supports a constructive medium-term view on small-cap equities. Nearly 40 percent of Russell 2000 companies carry floating-rate debt, meaning the lagged benefit of 2025 Federal Reserve rate cuts is still filtering through balance sheets.(8)

Domestic manufacturing reshoring, driven by tariff policy and supply chain reconfiguration, disproportionately benefits smaller companies with U.S.-focused operations. And the valuation spread between small- and large-cap equities, while narrowing, remains above historical norms, suggesting that the catch-up trade has further to run even after the recent all-time high.

1. FTSE Russell, June 2026 Semi-Annual Russell US Indexes Reconstitution, Press Release, May 22, 2026.

2. FTSE Russell, Russell Reconstitution June 2026: Larger Leaders, Stronger Small Caps, June 18, 2026.

3. Ibid.

4. Russell 2000 Weekly Market Review, June 19, 2026.

5. Columbia Threadneedle, Why Own U.S. Small Caps in 2026, June 17, 2026.

6. First Trust Advisors, SMID Earnings Persistence, June 2, 2026.

7. FTSE Russell, June 2026 Semi-Annual Russell US Indexes Reconstitution, Press Release, May 22, 2026.

8. CME Group, Russell 2000 Futures Analysis, June 3, 2026.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.