By Bill O’Grady and Patrick Fearon-Hernandez, CFA

(N.B. Due to the Fourth of July holiday, our next geopolitical report will be published on July 18.)

As is our custom, we update our geopolitical outlook for the remainder of the year as the first half comes to a close. This report is less a series of predictions as it is a list of potential geopolitical issues that we believe will dominate the international landscape for the rest of the year. It is not designed to be exhaustive; instead, it focuses on the “big picture” conditions that we believe will affect policy and markets going forward. They are listed in order of importance.

Issue #1: The Russia-Ukraine War

Russia’s invasion of Ukraine has become the world’s top geopolitical issue, with major implications for diplomacy, alliances, military development, energy and food prices, international trade and finance, and investment prospects. At the time of this writing, the Russian military continues to make slow, plodding progress toward its scaled-down goal of seizing Ukraine’s eastern Donbas region and southern coast. Because of continued leadership and operational errors, Russia is also taking heavy losses in troops and equipment. Ukraine’s smaller but highly motivated and well-led military continues to carry out modestly successful counterattacks as it receives more advanced weapons from the West. There is an increasing likelihood that the conflict will settle into a long war of attrition, including a Ukrainian insurgency in Russian-occupied areas, all of which could frustrate President Putin to the point where he formally declares war, calls a general mobilization, and/or turns to nuclear weapons. Of course, war can be fluid; the trends we see today could change quickly and in unexpected ways. However, if current trends continue, we see the following implications:

Near Term: Energy and Food. Since Russia and Ukraine are both major commodity producers, the war’s main impact on the rest of the world in the coming months will probably be continued supply disruptions for key materials like crude oil, natural gas, fertilizers, wheat, and sunflower oil. These supply disruptions can’t be offset quickly or easily. As companies dip into their stockpiles to make up for the lost supply, we think prices will continue to rise for a wide range of basic goods. That will likely keep consumer price inflation higher than it otherwise would be, forcing central banks to keep ratcheting up interest rates and selling off their asset holdings. High prices and rising interest rates will also threaten many political leaders, as discussed below.

Medium Term: Industrial Shifts. In the coming few years, we think the war will prompt lasting changes in the opportunities and threats facing certain industrial sectors. One example is the global defense industry. We think Russia’s aggression has scared Western policymakers so much that they will now embark on a sustained effort to upgrade their military forces. We expect the United States and its allies to hike their defense budgets by hundreds of billions of dollars per year. If total NATO military spending reached the same share of gross domestic product (GDP) that was common early in the Cold War, it would double to about $2.186 trillion per year. U.S. defense firms are likely to be the early winners because they have more advanced products to offer and more spare production capacity than allied firms. Another industrial shift will probably involve energy infrastructure. As countries in Europe and elsewhere work to wean themselves off Russian energy supplies, they are planning massive new investments in alternative pipelines, import terminals for liquified natural gas (LNG), and renewable energy.

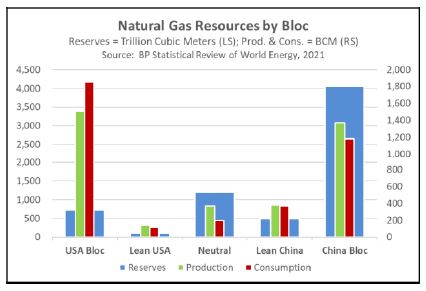

Long Term: Global Fracturing. We think globalization has been moving in reverse for years as U.S. voters have tired of their country’s traditional role as global hegemon. Now, the Russia-Ukraine war has accelerated the world’s fracturing into at least two major geopolitical and economic blocs, one led by the U.S. and one led by China. Driven by policies like the U.S. freeze on Russia’s international reserves and new trade restrictions against Russia, the countries coalescing into one bloc will erect many more barriers to trade, investment, and migration to and from the other bloc. Since these barriers will lead to short, inefficient supply chains, the process will keep costs higher than in the past and thus buoy inflation. That’s especially true for mineral commodities that aren’t evenly distributed around the world. Commodities controlled by the China-led bloc, such as natural gas and rare earths, are likely to be withheld from the U.S.-led bloc and become much more costly.

Issue #2: Xi as China’s President for Life

Russia sits at the top of our list of issues because it has attacked one of Europe’s biggest countries, creating a risky conflict with the U.S. and its democratic allies. Nevertheless, the world’s biggest long-term geopolitical issue is still China, its growing military and economic power, and the goals and intentions of its Communist Party leaders. Specifically, President Xi Jinping’s top goal in the coming months is to secure a precedent-breaking third term in office at the party’s 20th National Congress to be held sometime this fall.

In the leadup to the Congress, we expect that Xi will spare no effort to legitimize his continued rule. We expect him to focus on maintaining acceptable economic growth and ensuring political stability:

Economic Growth. In March, officials said they would work to ensure that Chinese GDP grows 5.5% in 2022. That’s the lowest Chinese growth target in decades, but it is widely seen as aggressive in light of the government’s strict “zero-COVID” policies and draconian lockdowns at even the slightest sign of infections in a community. Other headwinds include high global inflation, weak demand overseas, and the government’s effort to rein in big, powerful private firms in industries such as housing and high technology. Leading up to the party conclave, we already see signs that the government will try to spur more bank lending and greater investment, despite the impact on China’s steadily rising debt. The government has also eased some of its new regulations on tech firms. As of this writing, the moves have spurred a partial recovery in Chinese equity values, although we caution that those values could fall again after the assembly if an emboldened Xi decides to tighten his grip over the economy again.

Political Stability. Xi’s domestic political moves ahead of the Congress will probably focus on further pushing his nationalist “rising China, falling West” rhetoric, keeping a tight lid on new coronavirus infections, and maintaining his current strict social controls. The Chinese navy may launch its third aircraft carrier, which is currently nearing completion at a shipyard north of Shanghai (although the vessel probably couldn’t enter service until 2024). Since Xi was willing to double down on his draconian pandemic lockdowns in May and June despite the emergence of small popular protests against the restrictions, we judge that he wouldn’t hesitate to impose new lockdowns as necessary in the coming months, perhaps offsetting the resulting economic pain with still more investment stimulus and debt. Of course, doing so would increase debt risks in the future.

Issue #3: The Global Food Crisis

In our 2022 Geopolitical Outlook, we listed higher food prices as a potential geopolitical issue. This unfortunate prediction has come true to a degree we didn’t anticipate. The Ukraine war has disrupted the exports of wheat and edible oils from the Black Sea region, imperiling several nations.

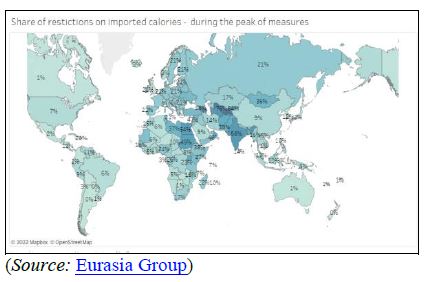

In the map below, the darker colors show which countries are most vulnerable to disruptions in the global food trade. The map indicates that Central Asia, Southeast Asia, the Middle East, and North Africa are all at serious risk of food shortages. Complicating matters further is the fact that Ukraine, Russia, and Belarus are major exporters of fertilizers. If alternative sources of fertilizer cannot be found, crop yields will suffer.

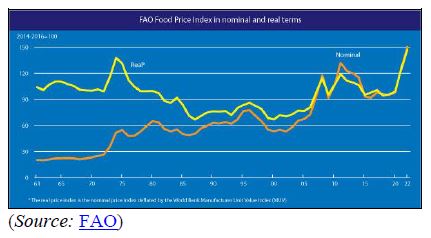

As shown in the following figure, the UN Food and Agriculture Organization’s food price index, which goes back to 1961, shows that current prices are at record levels on both a nominal and inflation-adjusted basis.

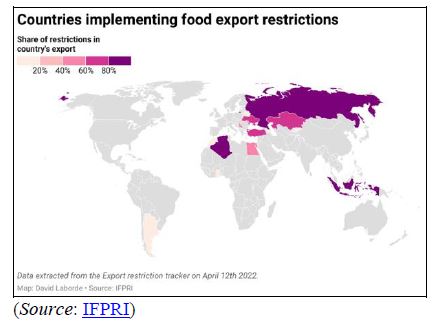

As shown in the next map, another disturbing trend is starting to emerge, where nations are restricting food exports to ensure that domestic populations will have enough food at tolerable prices. Although restricting exports is not necessarily a surprise, announcements of such actions tend to trigger panic buying. Hoarding behavior will likely exacerbate the impact of supply problems.

As the Arab Spring showed, food inflation raises geopolitical risk. Governments that can’t feed their people will likely see unrest. Food insecurity may also make it difficult for the U.S. and its allies to hold together the coalition aligned against Russia. If Russia can offer grain or fertilizer, the temptation to “run the embargo” will be strong.

Issue #4: Weather Disruptions

For farmers, weather is always a key factor in the success or failure of crops. But the majority of the time, weather problems tend to have mostly local effects. However, as globalization expanded, weather events began to have wider effects. The tsunami that affected Fukushima (though technically not a weather event) led to supply chain disruptions. Drought in Taiwan last year adversely affected semiconductor chip manufacturing. Australian wildfires in 2019 reduced agricultural exports.

For the rest of this year, there are two areas we are watching closely. First, given tight supplies in the grain markets, a drought in North America could be devastating for global food supplies. Generally speaking, U.S. corn and soybean crops are “made” from early July into mid-August. Sustained heat waves during this period could be problematic.

Second, natural gas has become much more of a global market due to the steady expansion of LNG. But the Ukraine war has put Europe in a vulnerable position as natural gas supplies from Russia contract. To support the EU, the U.S. has promised to boost LNG exports to the continent. These exports are vulnerable to two sorts of weather events. Hot weather in the U.S. will tend to boost demand for natural gas as the fuel is used to provide electricity. Exacerbating this problem is that the West is facing a drought, which is projected to reduce hydroelectric power. If the summer proves warmer than normal, it will create tight supplies given the promises of LNG exports.

A second weather factor that tends to affect LNG exports is tropical activity. In the U.S., tropical activity usually occurs from June 1 to November 1, peaking on average around September 15. NOAA is projecting an active season, with 14 to 21 named storms and six to 10 hurricanes. Hurricanes can cause disruptions in natural gas production, especially from offshore wells, but the advent of LNG exports adds a new dimension to the risk from tropical weather. The bulk of U.S. LNG export capacity exists in the Gulf of Mexico. Thus, any tropical activity in this region will almost certainly disrupt flows of LNG, even if the storm is small. A major hurricane could damage these facilities. Simply put, Europe, and to a lesser extent, Asia, could see a drop in supply during tropical events. Any LNG disruptions will put the EU at risk of shortages this winter and improve Russia’s position.

Issue #5: Latin American Politics

Against the backdrop of Russia’s war in Ukraine and the resulting disruption in global commodity supplies, Latin America’s big commodity producers would appear to be in a strong position to grab market share and take advantage of high prices. The issue spoiling this rosy picture is that the region will hold several major elections in the coming months that could lead to greater government intervention in the economy and a less attractive investment climate:

Brazil. On October 2, citizens will not only choose members of the National Congress, but they will also cast their first vote for president. If no candidate wins at least 50% of the first-round vote for president, the top two vote-getters will compete in a run-off on October 30. Current polling suggests leftist firebrand and former president Luiz Inácio Lula da Silva (“Lula”) would easily win the first and final rounds of voting, ending the rule of incumbent President Jair Bolsonaro, a right-wing populist whose standing has weakened due to scandals, pandemic missteps, and economic challenges. True to his leftist bona fides, Lula launched a range of popular social and anti-poverty programs in his two terms in office from 2003 to 2010, but strong Chinese demand for Brazilian commodities helped cover the cost and ensured good economic growth. With Lula in power again, the risk is that he would launch a new round of expensive programs or market interventions beyond what today’s high commodity prices could pay for.

Chile. On September 4, Chileans will vote on a new constitution. If passed, the draft law would replace a 1980 constitution widely credited with enshrining free-market liberalism and promoting economic growth. The proposed constitution would grant sweeping social rights to citizens, while dismantling many protections for businesses. For example, it would phase out protections for foreign investors in the country’s important mining industry. Current polling suggests a plurality of Chileans plan to vote against the new constitution but, given the intense social unrest and political protests that Chile has suffered over the last two years, we think there is still a substantial risk that the draft could be approved. Even if voters choose to keep the current constitution, Chile’s new leftist president, Gabriel Boric, has called for policies that would be decidedly negative for investors, including higher taxes to fund new social benefits, increased environmental regulations, and dismantling the country’s private pension system.

Issue #6: The U.S. Midterms

Midterm elections are usually unhappy affairs for the party in power. Presidential elections, especially for first-term presidents, are accompanied by great hopes for change. The party out of power is often questioning its future, trying to figure out why they lost, while the winning party celebrates. But after the euphoria wears off

and the hard work of governing begins, disappointment sets in. The U.S. is a two-party system that creates coalitions; differences between members are often “papered over” to win the election. Once in power, the differences reassert themselves and the party in power struggles to meet the internal demands of the party. Meanwhile, the party out of power usually coalesces in opposition, covering their own differences. And so, in most midterm elections, the party in power goes into the election divided and faces what appears to be a unified opposition.

The Democratic Party coalition appears frayed. High inflation is forcing the White House to accommodate the fossil fuel industry, much to the chagrin of the environmental wing of the party. The left wing of the party was hoping to remake American society. That effort has failed to materialize. On foreign policy, the Biden administration has been institutionalist, in opposition to the “America First” goals of the previous administration. This policy has led to a resurgence of alliances in both the Atlantic and Pacific, but also raises fears

that they won’t last past this administration.

A conservative forecast would lead one to expect the GOP to take control of the House of Representatives. Prediction markets are projecting a GOP takeover of Congress. The most obvious ramification of this

change in power is that passing legislation becomes close to impossible. To some extent, that is why equities tend to rally after the midterm elections as the chances decline for policy “volatility.”

The Biden administration has been supportive of the Ukraine war. U.S. actions have led to a surprising strengthening of NATO, with Finland and Sweden asking to formally join the treaty organization. Even Germany has moved to boost defense spending. However, there is an element within the GOP that has opposed further spending on the conflict. Although this opposition may change once the GOP holds legislative power, if the U.S. wavers in its support of Ukraine, divisions within NATO on supporting Kyiv will likely emerge.

It is apparent that there are divisions within Europe on the path forward for the Ukraine war. France’s recent comments about avoiding “humiliating” Putin stand in stark contrast to Kyiv’s goal of pushing Russian troops out of Ukraine. The economic disruption hitting Europe will likely lead to calls for a negotiated settlement.

As mentioned above, we think the Ukraine war has accelerated the restructuring of the world order that has been going on for the past decade. An end to hostilities, even if it seems premature to the Zelensky government, won’t likely change the direction of travel. But weakening U.S. support for the war after the midterms is a distinct possibility and hints at an evolving U.S. foreign policy that will likely be less hegemonic in the future.

Issue #7: Fed Policy and the Dollar

Inflation is quite elevated in the U.S. CPI is running at levels not seen in four decades. The White House has made it clear that it won’t interfere with Federal Reserve efforts to bring down inflation.

The “Volcker dollar,” which ran from 1980 to 1985, occurred in part because the Fed aggressively raised interest rates.

We don’t expect a repeat of those circumstances; not only was Volcker trying to snuff out inflation expectations, but the Reagan administration was cutting taxes. This meant monetary policy was also used to offset fiscal stimulus. Although we have seen historic fiscal expansion over the past couple of years, if anything, the fiscal situation (at least measured by the rate of change) is tightening.

What is worrying is that the U.S. is showing much greater austerity than other major currency nations. The Bank of Japan is maintaining its near-zero rate on 10-year sovereigns.

In addition, the European Central Bank (ECB) has indicated it will take steps to prevent “bond market stress,” which likely means it won’t let sovereign spreads become a problem. But that would likely require the ECB to expand its balance sheet. Simply put, the U.S. appears poised to implement relative austerity, which would be dollar bullish. And, since a stronger dollar does impede higher inflation, the Biden administration will likely allow it to rise further.

We would not expect dollar strength to persist indefinitely; by most measures, the dollar is richly valued. Nevertheless, as long as U.S. policy is focused on inflation reduction, dollar strength will be tolerated. In general, a stronger dollar will raise financial stress for the rest of the world. Under normal circumstances, dollar strength is bearish for commodities, but that may not be the case in the current situation due to the significant disruptions caused by the Ukraine war.

Quick Hits

This section is a roundup of geopolitical issues we are watching that haven’t risen to the level of the concerns described above but should be monitored. Some may be topics of future geopolitical reports.

- Tensions between Morocco and Algeria could disrupt natural gas flows to Spain. That event would exacerbate an already tight energy situation.

- Colombia is scheduled to hold a run-off presidential election on June 19. Although we don’t have the results to discuss in this report at the time of this writing, we note that it was contested by a leftist former guerilla, Gustavo Petro, and a right-wing populist with little political experience, Rodolfo Hernández Suárez. Either candidate could be unsettling for Colombian stocks.

Ramifications

Taken together, the issues we outline here will present both risks and opportunities for investors. With inflation driven not only by pandemic supply disruptions and excess liquidity, but also by the Russia-Ukraine war and faster deglobalization, there is a heightened risk that major central banks will tighten monetary policy too aggressively and spark financial instability or a recession. High inflation, rising interest rates, and a strong dollar create increased risk of economic or political instability in less developed countries, even as the commodity producers enjoy higher prices.

Against this backdrop of increased risks, our general approach to investment strategy recently has been to reduce our exposure to both U.S. and foreign equities and orient our remaining equity exposure toward value stocks. With bond yields now much higher than they were previously, we have increased our exposure to fixed income, but with an emphasis on government bonds rather than corporate obligations. Perhaps most importantly, we think today’s upward pressure on commodity prices will remain in place for the time being, so we have further increased our exposure to the commodity sector, especially in our more aggressive strategies. We also favor defense and aerospace due to expectations of higher defense spending.

This report was prepared by Bill O’Grady, Patrick Fearon-Hernandez, CFA, and Thomas Wash of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC

Confluence Investment Man agement LLC is an independent Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investm ent philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, company-specific approach. The firm’s portfolio management philosophy begins by assessing risk and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.