Politics is about what should be.

Investing is about what is.

It has always been important to separate one’s political views from one’s investment portfolio. Politicians’ goals typically attempt to support some vision of a better society. Investors’ goals are to maximize returns. These two goals can sometimes go hand-in-hand, but they often do not.

At RBA, we have portfolios that have specific mandates or guidelines outlining acceptable investments. Constraints such as minimum and maximum asset weights, volatility limits, country limits, or ESG restrictions are embedded in various RBA portfolios. However, where there aren’t such limitations, our sole goal is to aim for the best risk-adjusted return we can for our investors.

If investors give us a restrictive mandate, then we of course manage to that mandate. However, when there isn’t a restrictive mandate it is simply not our job to opine on politics.

For example, we were decidedly overweight Energy, Materials, and Industrials sectors as the global economy emerged from the pandemic despite some investors’ ESG concerns. Similarly, today we see significant opportunities in China despite some investors’ geopolitical concerns.

Our process leads us to China

Our investment process has for decades been based on examining three categories of data: corporate profits, liquidity, and sentiment/valuation. We look to invest in market segments in which fundamentals are improving, liquidity is growing, and are undervalued because investors are fearful. We try to avoid segments in which fundamentals are deteriorating, liquidity is drying up, and are overvalued because investors see little risk.

China increasingly fits the characteristics of an attractive market under our criteria: the Chinese profits cycle has likely troughed, China’s central bank is easing monetary policy, and valuations are depressed because investors strongly dislike China.

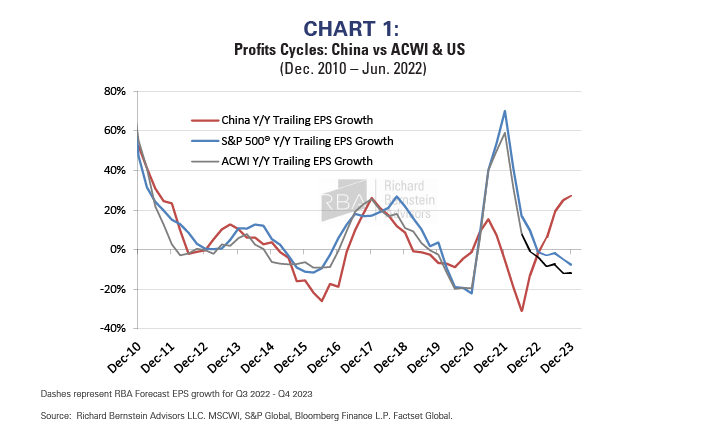

China Profits

Chart 1 highlights our view that China’s corporate profits cycle has likely troughed, whereas the US and global profits cycles seem ripe for continued deceleration. The US profits cycle is facing some strong headwinds through the end of 2022 and 2023. The strong US dollar, rising input and labor costs, poor productivity, and very hard comparisons versus 2021 and early-2022 are just some of the strongest challenges.

For China, however, the opposite could be true. The strong USD has led to a weaker CNY and China appears to be slowly emerging from their COVID lockdowns. If China does alleviate lockdowns even to some extent, then the end of 2022 and 2023 could see pent-up consumer and business demand growth similar to that seen in the US toward the end of 2020 and into 2021.

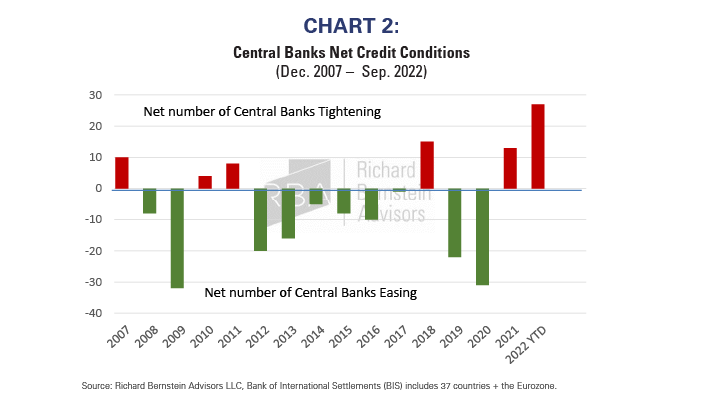

China Liquidity

Central banks around the world are largely in tightening mode. Chart 2 shows the net number of central banks tightening or easing monetary policy by year (i.e., the number tightening less the number easing). More central banks were tightening credit conditions when the bars were red, and more were easing when the bars were green.

Global central banks are clearly tightening largely because of their need to restrict credit as inflation has roared back during 2022. Credit conditions appear the tightest in the last 15 years when measured using this simple statistic.

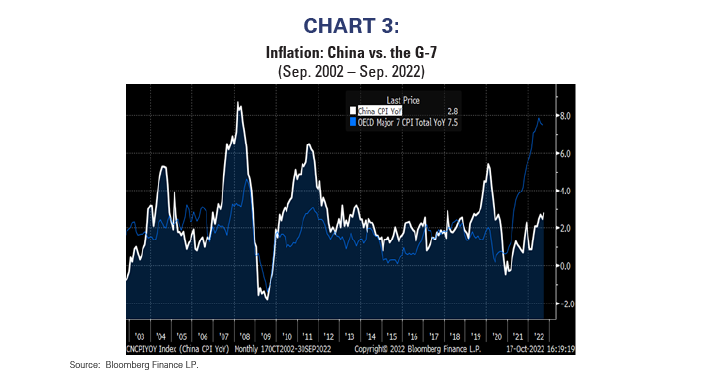

However, the People’s Bank of China is not yet burdened with having to fight inflation. Chart 3 demonstrates that China’s inflation rate is substantially below that of the G-7 countries. In fact, the G-7 inflation rate has never been this high relative to China’s during any time in the last twenty years.

Whereas western central banks are aggressively tightening credit conditions to fight inflation, China’s central bank is actually trying to add liquidity and stimulate growth.

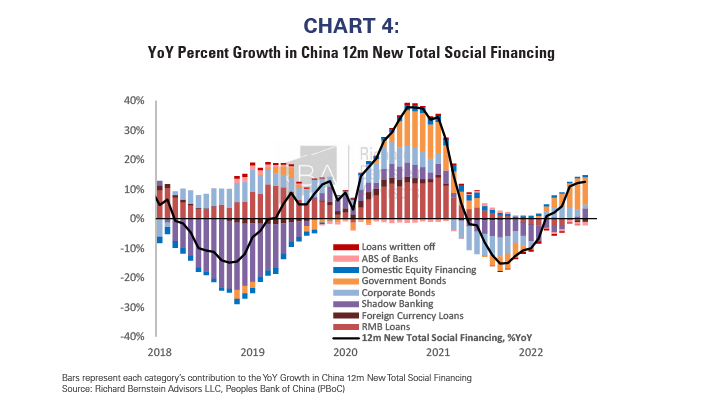

China’s credit cycle is on the upswing. Chart 4 shows the credit cycle’s upturn and shows how the composition of lending has changed through time. For example, this cycle is not being fueled by residential real estate lending.

Sentiment and Valuation

We group valuation among our sentiment indicators because it seems logically impossible to have a popular asset that is cheap or an unpopular one that is expensive.

Many investors have legitimate concerns regarding the Chinese economy, but one has to assess whether those concerns are well-known and already factored into asset prices. Chinese equity valuations suggest the widespread avoidance of Chinese equities is indeed reflected in prices.

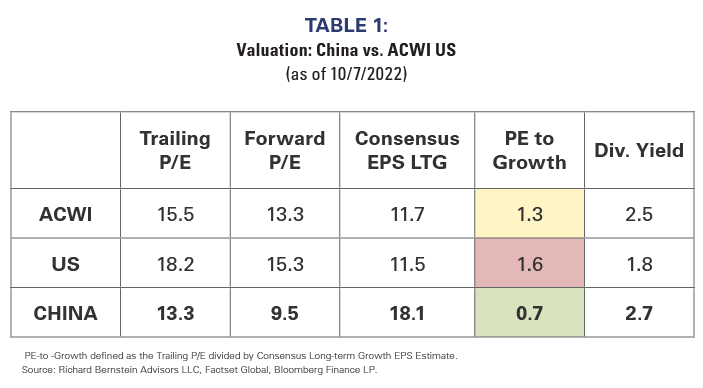

Table 1 compares several valuation parameters for the US, Global, and Chinese equity markets. China is the most undervalued regardless of the measure chosen. When compared to the US, China’s dividend yield is 50% higher and the PE-to-Growth Rate is less than half.

China certainly qualifies as an unpopular market.

Investors need to be dispassionate

It’s hard to follow a true investment process because there is always something or someone suggesting the process shouldn’t be used. Whether it is ESG or China, politics is now one of those factors attempting to pull investors away from discipline.

At RBA, we always follow our discipline based on profits, liquidity, and sentiment/valuation. Right now, that discipline is suggesting Chinese equities are steadily becoming more attractive.

For more news, information, and strategy, visit VettaFi.com.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.