EM FX Devaluations

An FT article caught our attention this morning – but it’s not the one about the sustainability of Japan’s central bank government bond purchases and potential changes in the yield curve control mechanism (YCC) under the new governor (albeit this might have very serious implications for global Fixed Income, especially Investment Grade instruments with their super-tight spreads). “Our” article talks about “a spate” and “a further slew” of emerging markets (EM) FX devaluations caused by the strong U.S. Dollar. We are not sure how well this characterizes EM, especially in light of strong performance of many EM currencies last year or a dramatic repricing lower of Asian interest rates. Further, letting currencies go while accelerating structural reforms and engaging multilateral financial support is probably the best thing that can happen to developing economies from the longer-term perspective. This is the lesson learned by their predecessors – many of whom are now “EM Graduates” – in the wake of the 1997/98 global financial crisis. Egypt is not doing this – yet – and therefore still strikes us as vulnerable to such episodes – it’s really a “classic” setup including the part about learning the hard way.

EM Structural Adjustment

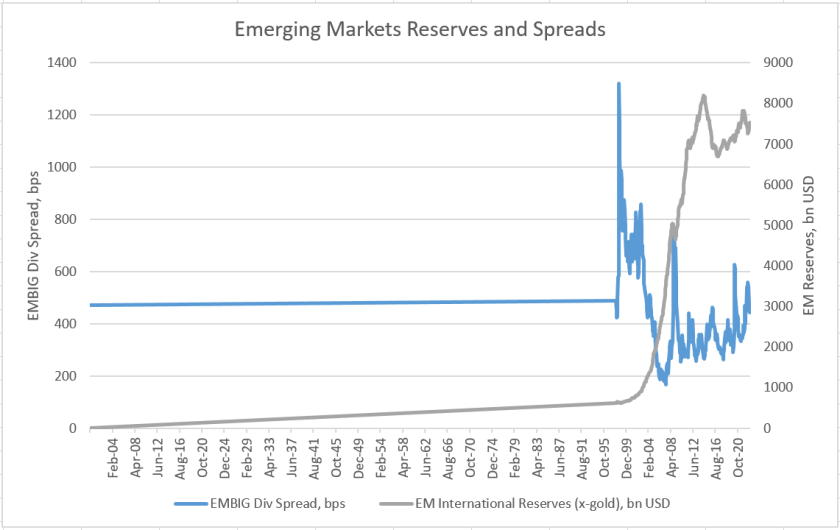

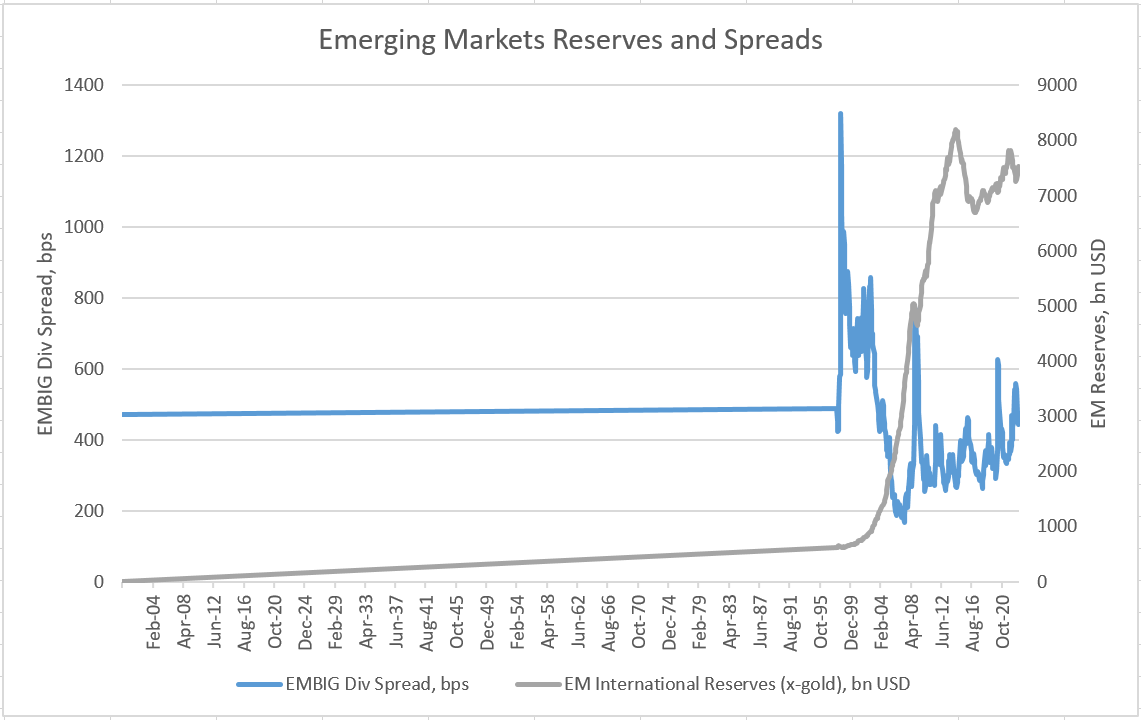

Using FX as a shock-absorber – while relying on interest rates as the primary policy instrument to target inflation – helps to initiate a “textbook” adjustment of the current account balance (less imports and more competitive exports). With fewer FX interventions, this is the fastest way to start rebuilding the international reserves. Over time, the accumulation of reserves and a stronger structural/institutional backdrop should lead to a major decline in sovereign spreads, limiting the extent of potential “flare-ups” in the future. The chart below demonstrates all these points very well (higher reserves/tighter spreads/lower peaks). Many EMs are now net sovereign creditors in U.S. dollars!

EM FX And U.S. Dollar

EMs that used their past devaluation experiences wisely – reforms, accumulation of reserves, inflation-targeting – are now less tied up to the U.S. Dollar cycle. The Brazilian real, the Mexican peso, the Peruvian sol, and the Chilean peso ended up stronger vs. the U.S. Dollar last year. The final point here is that there are different ways to get exposure to emerging markets these days. For example, we don’t like Brazil’s local market currently (due to policy noise), so we just don’t own it…but the current environment can still be positive for Brazilian credits that pay in real and earn in U.S. Dollar (for example). Stay tuned!

Chart at a Glance: EM Reserves vs. Sovereign Spreads in Different Regimes

Source: Bloomberg LP.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.