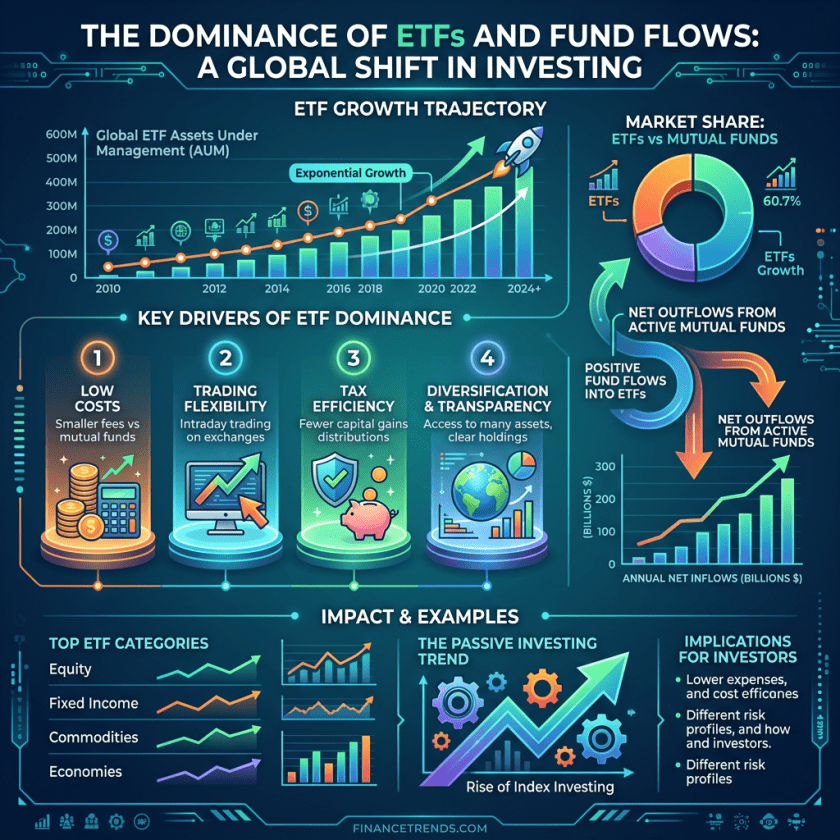

If there’s a single throughline connecting this week’s Investment coverage, it’s the steady consolidation of ETFs as the default building block of the modern portfolio. New ICI data shows the shift in stark terms: ETFs pulled in $32.3 billion in net inflows while mutual funds bled $28.87 billion, a trend detailed in The Great Migration: ICI Data Highlights Shift From Mutual Funds to ETFs, which credits lower fees, intraday liquidity, and tax efficiency for the migration. That preference is showing up further upstream too: Model Portfolios Gain Momentum in 2026: How ETFs Fit In reports model-portfolio assets climbing to $943 billion, up 46% year over year, with ETFs now representing 55.4% of the average model portfolio.

New product launches this week reflected where that appetite is heading. On the income side, Amplify Debuts New Dividend-Growth Strategy With DRVR rolled out a dividend-growth ETF built around a decade-plus track record of payout increases, while GUG: Worried About Inflation? Try Active Short Duration Bonds highlighted the Guggenheim Ultra Short Income ETF as a tool for investors bracing for stickier inflation. Elsewhere in fixed income, the case for looking further afield got a boost from Don’t Ignore the Potential of EM Bonds, which argues that emerging-markets debt, now more than a quarter of the global bond market, remains underrepresented in most portfolios despite improving credit quality.

Thematic ETFs also had a busy week. Capitalize on Fintech Disruption With the Active FDFF pointed to fintech firms using AI and machine learning to reshape banking, while No Mag 7? No Problem for Active Tech ETF GTEK showed that active management focused on smaller, innovative tech names has outrun the mega-cap-heavy benchmarks, up nearly 50% year-to-date. Energy infrastructure got its own spotlight too, with The Trillion-Dollar Midstream Opportunity laying out the case for $1.2 to $1.4 trillion in North American midstream investment by 2052, driven substantially by data-center power demand, a theme that dovetailed with Reactor Restarts Add New Layer to Nuclear Renaissance, which covered Holtec International’s milestone restart of a decommissioned reactor at its Palisades site.

Geopolitics reasserted itself in energy markets as well. Revival of Oil Turbulence Puts These Energy ETFs in Focus tracked renewed U.S. military action against Iran and a fraying peace deal, both of which pushed traders back toward leveraged energy plays like ERX and ERY. Meanwhile, sovereign capital kept accumulating power of its own: China’s SAFE Closes In On $2 Trillion Assets, Second SWF To Hit Milestone detailed how China’s foreign-exchange reserve manager is approaching the milestone with equities now making up 63.5% of its holdings, a notable tilt toward risk assets from a traditionally conservative allocator.

On the equity side, sentiment around Chinese tech stayed cautious. KWEB: World Class Tech Weighed By The China Discount noted the China internet ETF sitting near 52-week lows, down 28% year-to-date, with regulatory and geopolitical risk keeping the rating at HOLD despite long-term AI upside. That caution didn’t stop Cathie Wood just bought the SpaceX dip again, and dumped Alibaba to do it from making headlines, as ARK Invest trimmed its Alibaba position to add roughly $7 million of SpaceX shares, with Wood projecting a $3.1 trillion valuation by 2030.

AI itself remained the dominant undercurrent across markets. OpenAI Launches GPT-5.6 as Agentic AI Shifts ETF Outlook covered the rollout of OpenAI’s newest model family and its implications for tech-focused fund positioning, while the semiconductor angle came into sharper focus ahead of earnings: ASML Earnings Wednesday: EUV Bookings Will Show Whether the AI Chip Boom Is Sustainable framed ASML’s upcoming EUV bookings data as a key test of whether AI-driven chip demand can hold up, complicated by legislative changes affecting the company’s China revenue. That report set the stage for the broader corporate calendar: Q2 Earnings Preview: Tech & Energy Drive Growth Amid Healthcare Headwinds projects 23.3% earnings growth for the S&P 500 this quarter, led by technology and energy even as healthcare lags.

Taken together, the week’s coverage paints a market that is simultaneously chasing growth and hedging against its own momentum, piling into ETFs as the vehicle of choice for both, while watching inflation, oil, and AI chip demand for signs of whether the current run has further to go.

Full post index for this week:

- Don’t Ignore the Potential of EM Bonds · July 16, 2026

- KWEB: World Class Tech Weighed By The China Discount · July 16, 2026

- Model Portfolios Gain Momentum in 2026: How ETFs Fit In · July 16, 2026

- Cathie Wood just bought the SpaceX dip again—and dumped Alibaba to do it · July 16, 2026

- Amplify Debuts New Dividend-Growth Strategy With DRVR · July 15, 2026

- Reactor Restarts Add New Layer to Nuclear Renaissance · July 15, 2026

- GUG: Worried About Inflation? Try Active Short Duration Bonds · July 15, 2026

- OpenAI Launches GPT-5.6 as Agentic AI Shifts ETF Outlook · July 15, 2026

- Revival of Oil Turbulence Puts These Energy ETFs in Focus · July 15, 2026

- The Great Migration: ICI Data Highlights Shift From Mutual Funds to ETFs · July 15, 2026

- The Trillion-Dollar Midstream Opportunity · July 15, 2026

- China’s SAFE Closes In On $2 Trillion Assets, Second SWF To Hit Milestone · July 15, 2026

- Capitalize on Fintech Disruption With the Active FDFF · July 15, 2026

- Q2 Earnings Preview: Tech & Energy Drive Growth Amid Healthcare Headwinds · July 14, 2026

- ASML Earnings Wednesday: EUV Bookings Will Show Whether the AI Chip Boom Is Sustainable · July 14, 2026

- No Mag 7? No Problem for Active Tech ETF GTEK · July 14, 2026

Browse the full Investment archive at genesis-aka.net/investment/

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.