An editorial overview of the week’s key themes in Investment

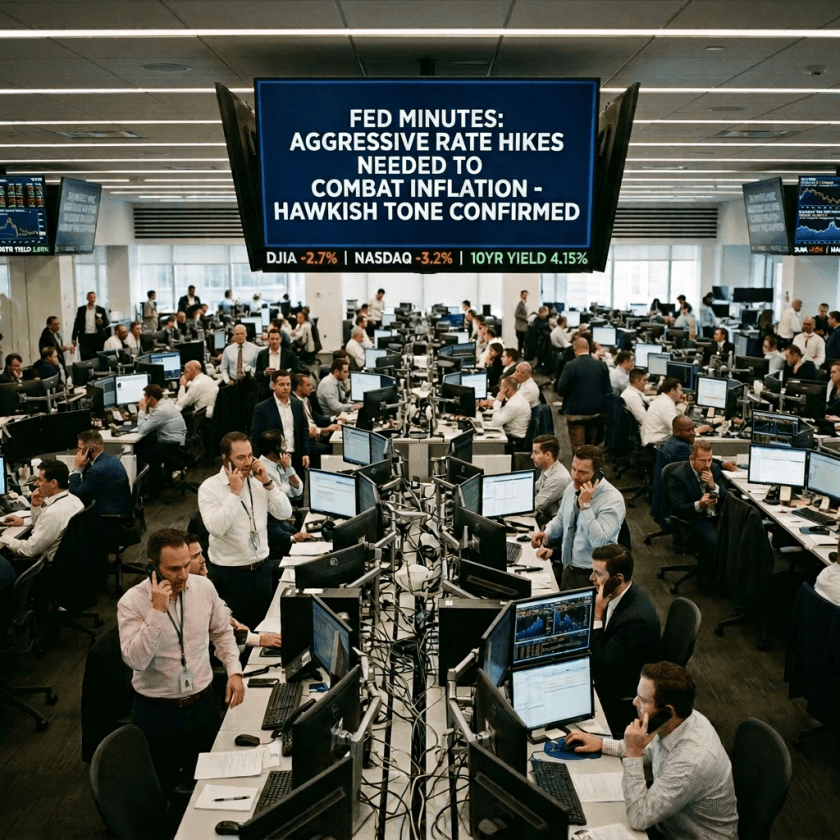

Markets spent this week absorbing a message the Federal Reserve seemed determined to keep brief. In The Fed Says Less, the June FOMC statement under Chair Warsh shed both word count and forward guidance, a hawkish-hold posture that leaves the door open to a rate hike before year-end. That kind of ambiguity tends to ripple outward, and this week it showed up first in how investors are re-pricing conviction bets in AI-adjacent equities. Nowhere was that more visible than in the reassessment of Nvidia, where an analysis identifying three key threats gaining momentum — customer-turned-competitor pressure, a slow migration away from GPU-centric compute, and mounting opportunity costs for holders — helped explain why shares have slipped from a $235 peak to around $192, even as the underlying business remains fundamentally sound.

That same skepticism toward star-driven AI narratives surfaced in two other stories. Wedbush’s Dan Ives, whose name anchors two thematic funds, departed the firm after eight years, and the resulting AI ETF power vacuum leaves investors in the Dan Ives Wedbush AI Revolution ETF and AI Power & Infrastructure ETF weighing whether to stick around without the strategist whose research underpinned them. Meanwhile, Michael Burry’s public short positions against names like Micron and Nvidia are drawing scrutiny for possibly moving markets on reputation alone — the piece on Burry’s own version of the ‘Buffett effect’ argues his disclosed bets may be triggering sell-offs somewhat independent of fundamentals. Taken together, these three stories point to a market growing more attentive to the personalities behind big AI calls, and more willing to question them.

Not every equity story this week was AI-anxious, though. Sector performance data showed real breadth: the roundup of top-performing sector SPDRs found Technology still leading 2026 gains at 33%, with Energy and Industrials putting up solid 21% and 20% returns respectively — evidence that despite the June wobble tied to macro jitters, more than one corner of the market is working. And the mechanics of how markets get measured are shifting too: the Russell 2000’s move to semi-annual reconstitution starting this June, replacing its old annual schedule, is designed to better capture small-cap dynamics and reduce unnecessary turnover — a structural change worth watching as the index’s earnings outlook improves.

On the fixed income and alternative-asset side, the week offered a case for looking past headline anxiety. The analysis behind the private credit chart nobody is paying attention to makes the point directly: redemption requests have climbed on AI-disruption fears, prompting some funds to restrict withdrawals, yet realized losses remain low — suggesting the market’s caution here may be running ahead of the actual risk, and quality lenders could be undervalued as a result. Dimensional Fund Advisors is making its own structural bet on fixed income, with a move to expand its ETF share-class push into bonds following its earlier pioneering of actively managed ETF share classes for equities. And further out on the alternative-asset spectrum, the case for gold mining’s next decade — a projected climb from roughly $293 billion to $808 billion in market size by 2034 — rests on rising ETF-driven investment demand and an increasing ESG focus, with growth increasingly concentrated in Africa and Latin America.

Global markets added their own reminder that index inclusion decisions carry real capital consequences. As Indonesia awaits an MSCI verdict on its market status, the country faces the prospect of up to $13 billion in outflows if downgraded, with persistent transparency concerns undercutting recent reform efforts and souring public sentiment in the process.

Amid all this macro and sector noise, two pieces this week brought the focus back to the individual investor’s plan. Advisors are being reminded of an overlooked opportunity inside workplace retirement plans: Self-Directed Brokerage Accounts let them manage client assets without triggering a rollover, yet remain underused despite their potential to deepen relationships and grow assets under management. And for those nearing retirement directly, the advice to build a one-to-two-year cash cushion before stepping away from work offers a concrete hedge against the kind of unexpected early exit that no amount of macro forecasting can fully protect against.

Put together, this was a week where confidence in easy narratives — a hawkish-but-quiet Fed, an unassailable AI trade, star strategists whose names alone move funds — came under quiet but real pressure. The more durable stories were structural: sector breadth beyond tech, fixed-income innovation, gold’s long growth runway, and the unglamorous discipline of retirement cash planning. Investors following this space would do well to separate the noise of personality-driven market moves from the steadier signals underneath.

Full post index for this week:

- As public sentiment sours, Indonesia awaits MSCI verdict which risks $13 billion in capital outflows · July 9, 2026

- Dan Ives Exits Wedbush: The New AI ETF Power Vacuum · July 9, 2026

- The Overlooked Opportunity Inside Workplace Retirement Plans · July 8, 2026

- The Private Credit Chart Nobody Is Paying Attention To, But Could Change Everything · July 8, 2026

- Top-Performing Sector SPDRs: XLK, XLE & XLI Top The List · July 8, 2026

- Why ‘Big Short’ investor Michael Burry may have his own version of the ‘Buffett effect’ · July 8, 2026

- As you approach retirement, take this simple step to protect yourself from unforeseen circumstances · July 8, 2026

- Dimensional Expands Share Class Push Into Fixed Income · July 8, 2026

- Gold Mining’s Next Decade: From US$293 Billion to US$808 Billion and What It Means for Investors · July 8, 2026

- Nvidia: 3 Key Threats Are Gaining Momentum And Visibility · July 7, 2026

- The Fed Says Less · July 7, 2026

- The Russell 2000’s First Semi-Annual Reset Signals A Deeper Small-Cap Evolution · July 7, 2026

Browse the full Investment archive at genesis-aka.net/investment/

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.