An editorial overview of the week’s key themes in Investment

This week’s Investment coverage kept returning to one uncomfortable question: who actually captures the value being created by the AI buildout? The week opened with a warning shot. SPX: Why Consumers, Not Profits, Will Win The AI Race argues that the S&P 500’s stretched price-to-sales ratio reflects AI optimism that history says will mostly accrue to consumers, not the companies doing the spending — and flags real risk of a correction if that pattern repeats. That thesis found a live case study in Amazon’s free cash flow collapse, where capex tied to AI infrastructure dragged free cash flow down to $1.2 billion even as operating cash flow rose 30%. The author still leans bullish, betting that AWS, custom silicon, and advertising eventually justify the spend — but the gap between cash generated and cash retained is exactly the dynamic the SPX piece warned about.

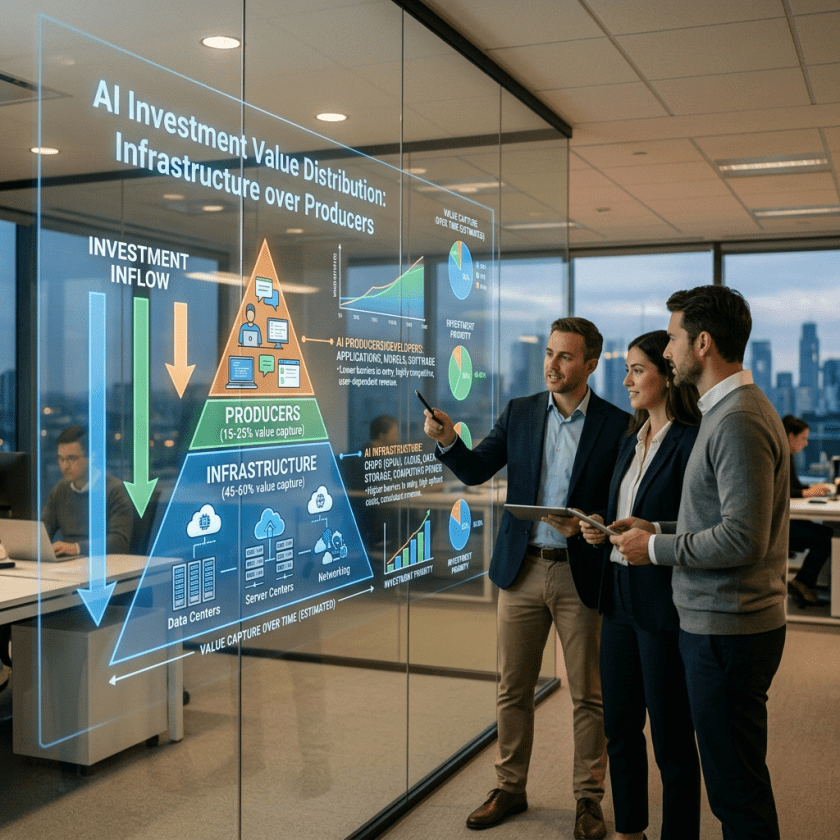

If producers are the uncertain bet, infrastructure suppliers looked like the more durable one. ELFY: Electrification ETF Bets on Power Grid Buildout makes the case for utility and grid companies feeding roughly 5% annual demand growth from EVs and AI data centers, rather than the tech firms consuming that power. It’s a “sell the shovels” argument, and it pairs naturally with open-source AI models eating the frontier, which tracked Zhipu AI’s GLM-5.2 release and Alibaba’s Qwen passing one billion downloads. As open models close the gap with proprietary ones, the value in AI increasingly looks like it migrates toward infrastructure, distribution, and adoption rather than toward whoever trained the biggest model first. China’s regulators are betting on a version of that same race: pre-profit IPO access for AI and quantum firms on the STAR Market, now live as of June 17, lets loss-making deep-tech companies list publicly under state approval criteria — explicitly using capital markets as industrial policy amid U.S. export restrictions.

On the fund side, the week’s theme was risk-adjusted selectivity rather than chasing the AI story directly. AMDL offers leveraged, 2x daily exposure to AMD on the agentic-AI server-stack shift, but the compounding mechanics of daily-reset leveraged ETFs make it a short-term trading tool, not a buy-and-hold position — a caveat the coverage was careful to underline. By contrast, IYZ’s stable cash flows from telecom carriers earned a buy rating precisely because it’s the opposite of exciting: mature carrier cash flow, modest appreciation, and dividend income, even if it has trailed peers like VOX and XTL. VBK, tracking 550 small-cap growth names at a 0.05% expense ratio, got a more mixed review, with the analysis pointing to competitor FYC as a potentially stronger long-term alternative despite VBK’s scale and low cost.

That preference for proven over speculative also ran through why first-mover advantage matters for active ETFs, which noted that active ETFs accounted for 80% of 2026’s launches through May, yet most still lack even a three-year track record. The piece holds up American Century’s lineup as evidence that being early and building a real performance history beats simply being new, and suggests investors weight seasoning heavily when sorting through the current flood of active launches.

Taken together, the week’s nine pieces sketch a market still committed to the AI buildout but increasingly skeptical about where the payoff lands. The S&P 500 and Amazon stories question whether AI capex converts into producer profit at all; the electrification and open-source pieces suggest the more reliable winners are infrastructure and distribution rather than the frontier labs themselves; and China’s IPO rules show regulators racing to capture upside before profitability even exists. Meanwhile the fund coverage — AMDL’s leverage warning, IYZ’s boring-is-good case, VBK’s mixed marks, and the active-ETF track-record argument — points toward the same conclusion from a different angle: as the AI cycle matures, discipline and proven history are being rewarded over momentum and novelty.

For investors, the throughline this week is less “is AI real” and more “who gets paid for it.” The consumer-surplus argument, the capex-versus-cash-flow tension at Amazon, and the bet on grid and open-source infrastructure all point toward looking past the most obvious AI tickers and toward the suppliers, distributors, and disciplined funds positioned to benefit regardless of which model or company wins the frontier race.

Full post index for this week:

- SPX: Why Consumers, Not Profits, Will Win The AI Race · June 24

- AMDL: Agentic AI Is Shifting The Server Stack, Amplify Your AMD Exposure At The Inflection Point · June 24

- Open-Source AI Models Are Eating the Frontier: Where Value Goes · June 24

- China Expands Pre-Profit IPO Access to AI and Quantum: STAR Market Rules Now Live · June 23

- ELFY: Electrification ETF Bets on Power Grid Buildout · June 23

- Amazon: I’m Buying The Free Cash Flow Collapse · June 23

- IYZ: Stable Cash Flows From Telecom Carriers And Fiber Expansion · June 23

- VBK: The Growth Factor Is Less Compelling In Small Caps · June 23

- Why First-Mover Advantage Matters for the Best Active ETFs · June 22

Browse the full Investment archive at genesis-aka.net/investment/

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.